Shifts in the Fed’s dot plot should set the market’s tone

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- The Fed’s easing cycle will begin next week

- Shifts in the dot plot should set the market’s tone

- Fed rate cuts have historically been positive for equities

The time has come! After the most aggressive tightening cycle in modern history, the Fed is ready to turn the page and begin dialing back its policy restraint after the second longest ‘on hold’ period (14 months) in history. Barring any surprises, the Fed should lower interest rates at its meeting next week—the first rate cut in over four years—in the hopes of preserving a soft landing for the economy. While the pace and magnitude of the Fed’s upcoming easing cycle remain in flux (we expect the Fed will start with a 25 bp cut), all eyes will be on the Committee’s economic forecasts and the Fed Chair’s press conference for clues on how things will evolve. Below we preview how the Fed’s economic projections and dot plot may shift and what impact the upcoming easing cycle could have on the fixed income and equity markets.

- Updated Economic Projections | Thus far, growth has remained steady—supported by slowing, but still solid consumer spending. In fact, the Atlanta Fed’s Q3 GDPNow is currently estimated at 2.5%—hardly signaling any signs of a recession. With growth still modestly above trend, the Fed is likely to push its 2024 growth forecast (2.1%) higher, while leaving 2025 (2.0%) intact. However, one area of softening has been the labor market as seen by the steady climb in the unemployment rate (4.2%) and the slowing pace of job growth—with the 3-month moving average decelerating to a 116k per month pace versus the 267k pace in March. Cooling, but certainly not collapsing. With the unemployment rate above the Fed’s 2024 year-end forecast (4.0%), expect a modest upward revision for this year and next. Inflation has also decelerated more quickly than the Fed expected (aided by falling oil prices), so expect small downward revisions to its 2024 (2.8%) and 2025 (2.3%) inflation estimates.

- New Dot Plot | While the Fed’s economic changes should be minor, the dot plot shifts will set the market tone. The Fed is likely to increase the number of rate cuts in 2024 (from 1 expected in June), but not be as aggressive as the 100 bps of easing the market is expecting by year end. In June, the median dot for 2025 centered on 4.1% with 15 FOMC members expecting the fed funds rate to be above 3.0% in 2026—still above the Fed’s estimated long-term neutral rate of 2.8% (i.e., a level that neither stimulates nor restricts growth). With economic activity only modestly slowing (Visa’s Spending Momentum Index suggests August spending bounced back) and job growth still positive, the Fed will likely maintain a gradual approach to rate cuts—maintaining firepower if employment or growth momentum stall. A less aggressive Fed rate outlook could spark some volatility given market expectations.

- Powell’s Press Conference | We expect the Fed to deliver a 25 bp rate cut (rather than 50 bps) next week. Chair Powell should strike a dovish tone when he takes the podium to balance the market’s optimistic expectations. While not fully committing to the pace of future rate cuts and reiterating its data dependence, Chair Powell ought to repeat (consistent with his messaging at Jackson Hole a few weeks ago) that the downside risks to a slowing labor market (i.e., sluggish hiring, falling job openings), a softening consumer and easing inflation pressures are consistent with further easing by the Federal Reserve.

- Asset Class Impact | Below we outline our views on how the Fed’s easing cycle may impact the equity and fixed income markets:

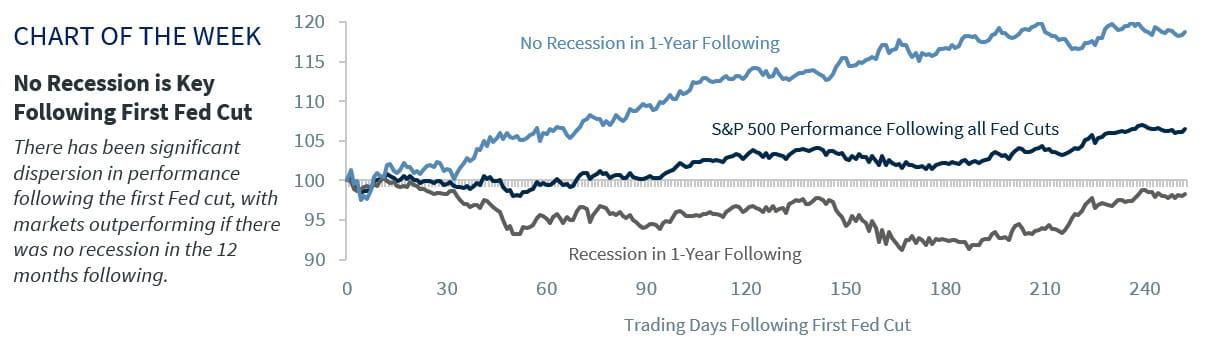

- Equities | Fed rate cuts have historically been positive for the equity market, as the S&P 500 is up 5% and positive 66% of the time in the 12 months preceding the first Fed cut. However, there is significant dispersion dependent on the macro backdrop. If Fed cuts stimulate economic growth that helps avert a recession in the following 12 months, the S&P 500 is up 18% on average, vs. a decline of 5% if the economy succumbs to a recession. With a soft landing, our base case, Fed cuts should provide a favorable backdrop for equities. From a sector perspective, defensive sectors have outperformed over recent weeks as the decline in long-term interest rates has boosted these sectors. However, as the bulk of the long-term interest rate declines are behind us, we caution investors on chasing performance in these areas as much of the good news has already been priced in.

- Fixed Income | Bond market moves have anticipated the Fed’s easing cycle—something we have been expecting for a while. However, given the 10-year Treasury yield is hovering below our mid-year 2025 3.75% target and the market is pricing in an aggressive, front-loaded easing cycle, bond valuations are not as compelling as they were a few months ago. Thus, the scope for significant capital appreciation from current levels is limited. However, given a slowing economy, yields should remain near current levels, generating reasonable income for investors. However, if there is another economic ‘growth scare,’ yields could head even lower. In the meantime, any rise in yields toward 4% should be viewed as an opportunity to modestly extend duration, particularly as bonds have resumed their role as a valuable diversifier and hedge to equity risk.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.