The Week in Review: 9/24/2024

“The line between failure and success is so fine. . . that we are often on the line and do not know it.” -Elbert Hubbard

Good Morning ,

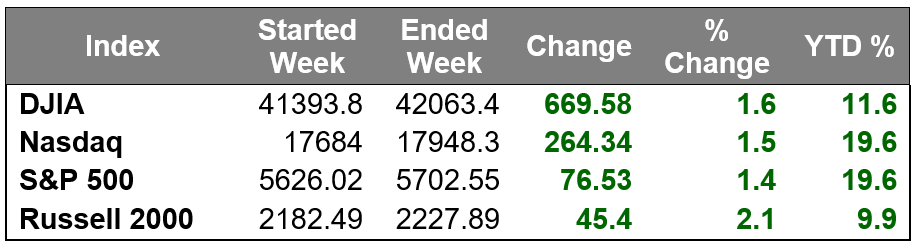

It was another strong week for stocks.

Early in the week, gains were fueled by optimism about the Fed cutting rates by 50 basis points. The Fed delivered and gains continued until Friday, when the market closed flattish as participants digested the solid week in equities.

Friday's session was also a "quadruple witching" quarterly expiration of stock options, index options, single stock futures, and index futures.

The Federal Open Market Committee (FOMC) voted in favor of cutting the target range for the fed funds rate by 50 basis points to 4.75-5.00%. It was not a unanimous vote.

Fed Governor Bowman preferred a 25-basis points rate cut.

The directive indicated that the Committee has "gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance."

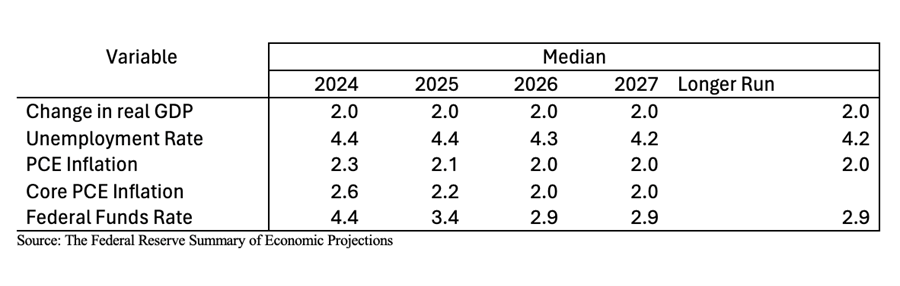

The Summary of Economic Projections showed a shift in the median estimate for the 2024 unemployment rate to 4.4% (from 4.0% in June) and a downward shift in PCE inflation to 2.3% (from 2.6% in June) and core-PCE inflation to 2.6% (from 2.8%).

The dot-plot, meanwhile, shows a median estimate for 2024 (4.40%) that implies another 50 basis points of rate cuts this year and another 100 basis points in 2025.

Fed Chair Powell defended the larger, 50-basis points cut as a proper "recalibration" to make sure the labor market and the economy remain in a solid condition and that the intent of the more aggressive move is to make sure they remain there.

He also said that the Fed doesn't feel like it is behind the curve with its policy rate and that the larger cut can be construed as a sign of the Fed's commitment not to get behind.

This thinking drew in buyers, along with a fear of missing out on further gains, and the S&P 500 and Dow Jones Industrial Average reached fresh record highs in the wake of the Fed's latest decision.

Last week's data largely corroborated the market's thinking that the Fed can orchestrate a soft landing for the economy. Retail sales and industrial production were both stronger than expected in August, weekly jobless claims remain steady below recession-like levels, and the Philadelphia Fed Index tipped back into expansion (i.e., above 0.0 reading) in September.

We also gained insight into the Fed’s outlook for the rest of 2024 and beyond in terms of how it views economic growth, inflation, and a projected policy path.

According to the quarterly Summary of Economic Projections, the Fed is estimating that the federal funds rate will conclude the year at a range of 4.25-4.50%, another 0.50% lower than it is currently. This suggests one more oversized 0.50% cut or two 0.25% cuts to conclude the year.

Only three S&P 500 sectors settled lower. The defensive-oriented health care (-0.6%) and consumer staples (-1.2%) sectors were among the laggards. Meanwhile, the energy (+3.8%), communication services (+3.7%), and financial (+2.4%) sectors were the top performers.

Market Snapshot…

- Oil Prices – Oil prices dropped on Friday but recorded a second week of gains. West Texas Intermediate crude was down 3 cents or 0.4% to settle at $71.92 a barrel, while Brent crude futures were down 39 cents, or 0.52% to $74.49 a barrel.

- Gold– Gold prices soared above $2,600 on anticipation of further rate cuts. Spot gold was up 0.3% to $2,593.80 per ounce. U.S. gold futures rose 1.2% to $2,643.30. Silver closed the week at $31.505.

- S. Dollar– The dollar hit its highest level in two weeks after the Bank of Japan left interest rates unchanged. The dollar was up 0.92% to 143.92 while the dollar index gained slightly to 100.75. Euro/US$ exchange rate is now 1.114.

- S. Treasury Rates– The U.S. 10-year Treasury yield fell about 1 basis point at 3.732% but was higher by almost 8 basis points for the week even after the Fed lowered rates by a half point percentage on Wednesday.

- Asian shares were mostly higher in overnight trading.

- European markets are trading up.

- Domestic markets are trading up again this morning.

This week, several Fed speakers will be on the docket and may be giving clues into how specific individuals foresee policy changing in the coming months.

We will also receive a plethora of housing data. With mortgage rates now the lowest since early 2023, we will see if home sales pick up. Lastly, we will receive the final look at second quarter GDP and August’s PCE report.

Have a wonderful week!

Michael D. Hilger, CEP®

Managing Director

Senior Vice President, Wealth Management

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.