First Half Recap

First Half Market Notes, Consider the Roth 401(k), and Three Things for Q3

First Half Recap

With 2023 at the halfway point and markets off to a roaring start, let’s look back at what segments of the market fueled the rally.

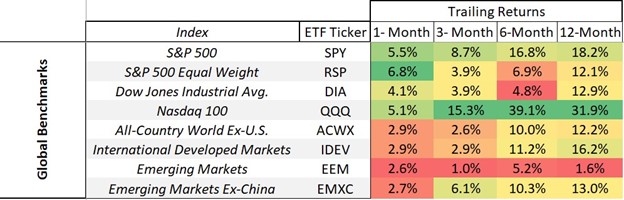

Global Benchmarks

Source: FactSet, Glacier Advisors of Raymond James

Notes:

- The Nasdaq 100 (ETF Ticker: QQQ), 2022’s biggest loser in the U.S., reversed trend and powered past its peers in the first six months. During a market recovery, it is often the oversold stocks that provide the strongest returns.

- A rate hike pause and easing inflation contributed to outperformance in the tech-heavy index.

- ChatGPT and AI supplied a wealth of returns for companies at the forefront of the artificial intelligence boom.

- The largest stocks in the S&P 500 contributed the most to the index’s returns.

- The S&P 500 is a market cap weighted index, meaning it gives a higher weighting to bigger companies. The S&P 500 Equal Weight index takes all stocks in the index and gives them an equal weighting.

- When the S&P 500 (ETF Ticker: SPY) outperforms the S&P 500 Equal Weight (ETF Ticker: RSP), it tells us that the biggest companies, not the average-sized firms, are driving market performance.

- International markets participated in the recovery, but Emerging Markets (ETF Ticker: EEM) lagged.

- A stalled economic recovery in China contributed to the relative underperformance.

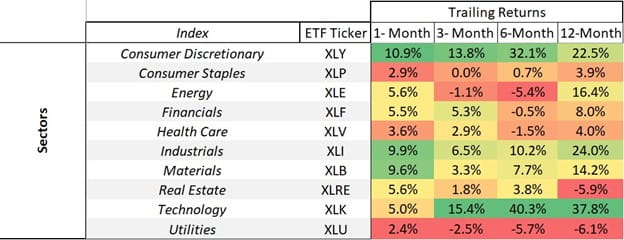

U.S. Sectors

Source: FactSet, Glacier Advisors of Raymond James

Notes: Last year’s lagging sectors are leading the recovery.

- Technology and Consumer Discretionary take the crown for best performing sectors in the first half.

- These sectors underperformed the markets in 2022. o The largest U.S. companies like AAPL, MSFT, AMZN, and NVDA boosted returns for the sectors.

- Large investments poured into AI pioneers like MSFT and NVDA.

- Sectors that investors consider to be “safe” during market downturns provided negative returns throughout the first half.

- Utilities, Healthcare, and Staples are not participating in the recovery of 2023.

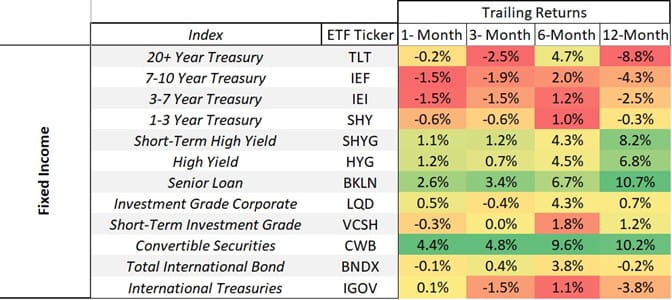

Fixed Income

Source: FactSet, Glacier Advisors of Raymond James

Notes:

- Treasuries continue to struggle relative to the rest of the bond market.

- Uncertainty around the interest rate path led to volatility in treasury markets.

- Higher-risk bonds that are tied to economic strength performed best.

- High Yield (ETF Symbol: HYG), Senior Loan (ETF Symbol: BKLN), and Convertible Securities (ETF

Symbol: CWB) represent fixed income securities that carry more economic risk relative to peers.

Consider the Roth 401(k)

The Roth 401(k) is an underutilized tool offered by most employer sponsored 401(k) plans. Unlike the Roth IRA, the Roth 401(k) has no income limits. Meaning anyone can contribute from their paycheck, regardless of income levels. It offers tax advantages that can benefit individuals in the long run. Contributions to a Roth 401(k) are made with after-tax dollars, meaning that you pay taxes on the money upfront. However, the growth and withdrawals from the account are tax-free, provided certain conditions are met. This is advantageous for individuals who anticipate being in a higher tax bracket during retirement, as they can effectively lock in their current tax rate and potentially save on taxes in the future.

Also, the Roth 401(k) provides flexibility in terms of withdrawals. Unlike a traditional 401(k) where withdrawals are subject to income tax, withdrawals from a Roth 401(k) are tax-free if the account has been held for at least five years and the individual is at least 59½ years old. This can be beneficial for retirement planning, as it allows individuals to strategically manage their income and potentially reduce their tax liability during retirement. Additionally, the Roth 401(k) does not have required minimum distributions (RMDs) during the account holder's lifetime, which provides more control over the timing and amount of withdrawals, allowing for potential tax and estate planning advantages. Overall, the Roth 401(k) offers a unique combination of tax benefits and flexibility, making it a valuable option for individuals looking to optimize their retirement savings strategy.

Three Things for Q3

1. Check your savings goals – Inflation took a chunk out of everyone’s wallet. Are you saving the amount you had hoped for? Do you need to make spending adjustments? Given the historically high inflation rates of the last two years, its worth taking a look at what costs are effecting you most.

2. 529 College Savings Plans Just Got Better – new tax rules passed in the Secure 2.0 Act enhanced the benefits of 529 college savings plans. Starting in 2024, 529 account holders will be able to transfer up to a lifetime limit of $35,000 to a Roth IRA for a beneficiary. Unused college savings funds transferred into a Roth IRA provide a unique savings and gifting tool for investors - providing tax-free growth.

3. Money Market Accounts – many banks still provide inadequate yield on your checking and savings accounts. Consider different types of money market investments or short-term treasuries. Many of these products provide over 5% returns with little to no risk.

We expect uncertainty to persist in markets and all eyes remain on the Fed and its rate hike campaign. So far, the United States sidestepped the widely predicted recession. Watch for key indicators like improving GDP, declining inflation, and strength in the Equal Weight S&P 500 Index. The team at Glacier Advisors of Raymond James monitors the data to make careful decisions to help defend and grow client’s wealth. Continue to review your financial plan with your advisor and most importantly, assess your risk tolerance after enduring a tough 2022. Make the necessary adjustments. We look forward to continuing to serve for the rest of 2023 and beyond!

- Scott Miller – Senior VP, Investments

- Brett Miller, CFA, CFP® - Financial Advisor

Any opinions are those of Scott Miller and Brett Miller and not necessarily those of Raymond James. This information is intended to be educational and is not tailored to the investment needs of any specific investor. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance is not indicative of future results.

Every investor's situation is unique, and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. You should discuss any tax or legal matters with the appropriate professional. Chart are for illustration purposes only and not a recommendation.

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results.

Roth 401(k) plans are long-term retirement savings vehicles. Contributions to a Roth 401(k) are never tax deductible, but if certain conditions are met, distributions will be completely income tax free. Unlike Roth IRAs, Roth 401(k) participants are subject to required minimum distributions at age 72 (70 ½ if you reach 70 ½ before January 1, 2020).