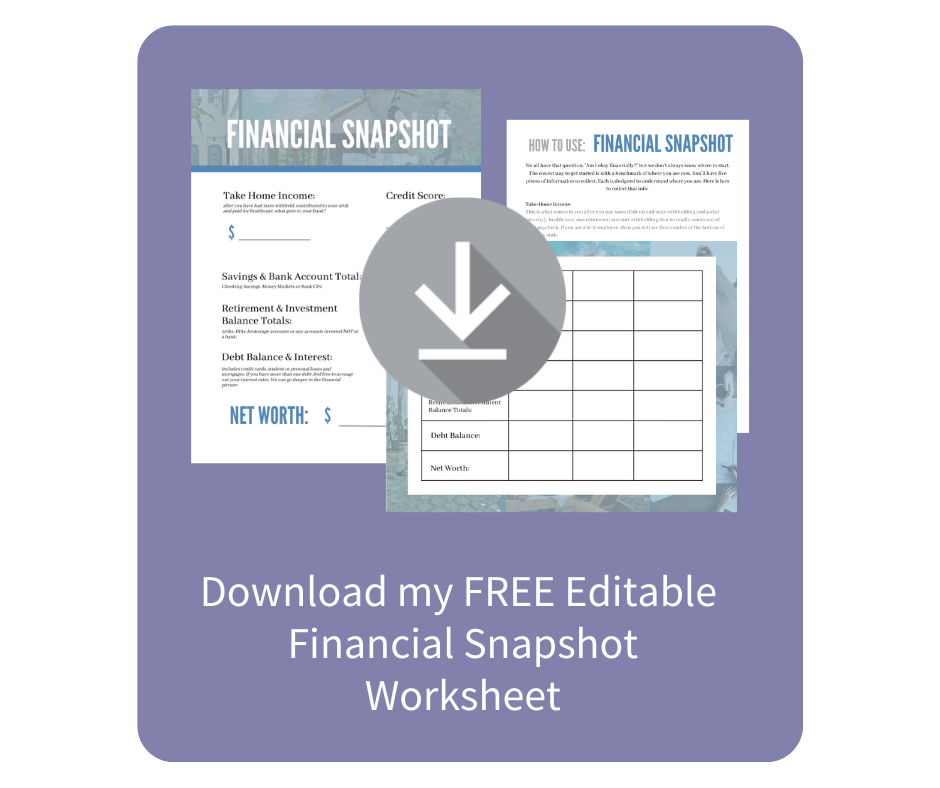

The Basic Financial Snapshot

Let’s get down to business. You’re here because you want to know…

AM I OKAY?

As a young and growing family, it can feel even like you're paycheck to paycheck, even as a professional working their butt off.

So, what is normal?

How can you tell if your finances add up?

Those are questions that most successful women I work with are looking to answer, but the secret is; “Okay” looks different for everyone.

Okay for you, is better than yesterday or last week, and the metrics we measure it by are:

- Take Home Income

- Savings

- Debt

- Credit

- Retirement & Investments

So, regardless of your situation, knowing how you stack up to your previous self, and the person you want to be (maybe with a second home built for relaxing?) will be the first step toward achieving your financial goals.

TAKE HOME INCOME

This is the money that you bring home AFTER taxes and healthcare, etc. This is what hits your bank each month. If you are not on salary, it is a little more difficult to calculate that information.

As an employee, this is found on your pay stub- you can take a look at what comes out and what you are paid.

As an employER or self-employed, it can be a little more difficult to find this number, but your CPA or this article should be able to help.

INCOME LEVERS:

- Spend less / make more

- Taxes – speak with your CPA to confirm that your withholding makes sense

- Retirement accounts – up/down contributions

SAVINGS

What are your balances at your bank, credit union or anywhere you are holding cash or what can be used as cash? Right now, you don’t need to break it up by how much is where, but if you have the data, GREAT- Hang on to it. If not, here are a couple of examples of what I consider cash.

- Checking, savings, and money market accounts at banks or credit unions

- Cash Under your bed or in a safe

- Bonds at Treasury Direct

SAVINGS LEVERS:

- Consolidate – if you have a bunch of accounts, odds are that you forget about cash in some and it isn’t working for you OR you are paying more fees than you would with fewer accounts.

- Reduce the numbers of accounts and take full advantage of the highest interest rate.

- Unclaimed property search- in NC, where I live, there is a property search run by the state treasury. Find what you’ve lost.

DEBT

Do you have a mortgage? Student loans? Credit Card or Personal Loan debt? Make a tally of how much you owe and the average interest rate (we will go more in depth later). Again, if you have it, great, hop on over to the advanced financial snapshot and get started there. You are an overachiever!

- Credit Cards

- Student Loans

- Mortgage or Auto Loans

- Personal Line of Credit

DEBT LEVERS:

- Pay on different loans differently.

- Higher interest first (Avalanche Method)

- Lower balances first (Snowball Method)

- Consider debt consolidation - if you have a bunch of accounts with high interest, there are options that may offer you a chance to pay less overall. It also may make you unable to take government aid or other options should they present themselves.

- Refinance – if financers are offering a lower price for you to borrow, it may make sense to refinance and pay less over time, however, most lenders will charge a fee for this service that makes this option less desirable.

CREDIT SCORE

What is your credit score? It is a number that represents how likely you are to pay back any money you borrow. This is a huge part of getting an understanding of where you stand in lender’s eyes.

You don’t have to have a great credit score to be good with money, but it helps.

- Many credit cards show what you get when they pull your credit quarterly.

CREDIT SCORE LEVERS:

- Utilize your current line of credit more / less

- Credit companies reward those who live under their means. The closer you are to your credit limit you are on a regular basis, the lower your credit score will be.

- Pay balance on / before statement date

- Paying multiple times a month, and in full will improve credit scores. Conversely, if you pay the minimum, or anything less than your full balance, your credit score could be damaged.

RETIREMENT & INVESTMENTS

Do you have retirement accounts – 401k, IRA, etc? How about brokerage accounts or savings for a child’s college. This is the kind of account that can make (or lose) you money while you sleep.

- Brokerage, Joint or Trust accounts at an Investment Firm.

- 401k, 403b, 457s or any pensions or any other work retirement benefits.

- IRAs, Roth IRAs, SEP IRAs or other retirement accounts that you have full control over.

- And many, many more…

INVESTMENT LEVERS:

- Invest Regularly / Sporadically

- When you can, if you can automate adding in money

- Increase / Decrease your investment budget

- Sky is the limit. Your lifestyle can be your best friend or your worst enemy.

- Increase / Decrease the risk of your investments

- High risk can sometimes translate to high reward, but it can also mean your portfolio takes a big hit in a volatile or down market.

Okay, great, now that you’ve got a sense of what is where, you know where you need to focus your energy.

Make an appointment with yourself 3, 6, or 12 months into the future to see where you are and how you’ve improved!

Having trouble?

Pro Tip: This isn’t meant to be a laborious undertaking. Set a timer for 15 to 20 minutes, grab a pen, and do what you can. No shame if it isn’t everything.

Take it one step at a time until it is done!

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.