Shaking My Head

To watch/listen to this week’s article please click here.

Usually I would write to you stating that there was a ton of news that moved the market. Last week we continued to get market volatility, without a whole lot of new news. Fed Chair Powell spoke through the week, which is usually fraught with major swings. However, that move was limited to less than 1% and settled back to pre-press conference level fairly quickly.

The big move last week was within the market early on the week was led by the lagging sectors. Financials, Industrials and Energy boosted the market around 1000 Dow points on Friday (5th June), and validated on Monday (8th June) with another 600. To get back to new highs and beyond, the overall market will need these laggards to catch up and at some point, lead the other sectors. These sectors are classified as cyclical sectors, (which I discussed a couple of weeks back, click here). Cyclicals are closely related to the overall economy and benefit when the economy is string and growth is plentiful.

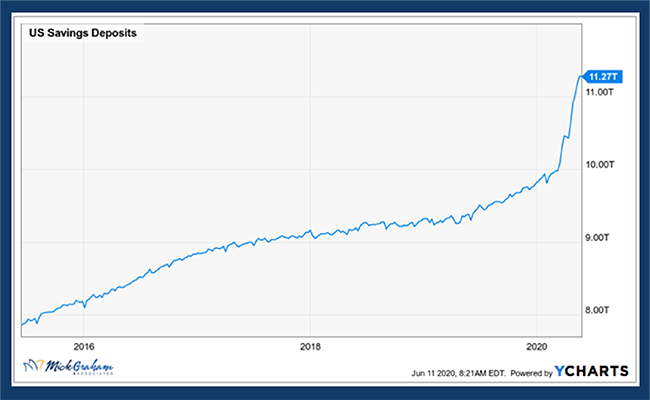

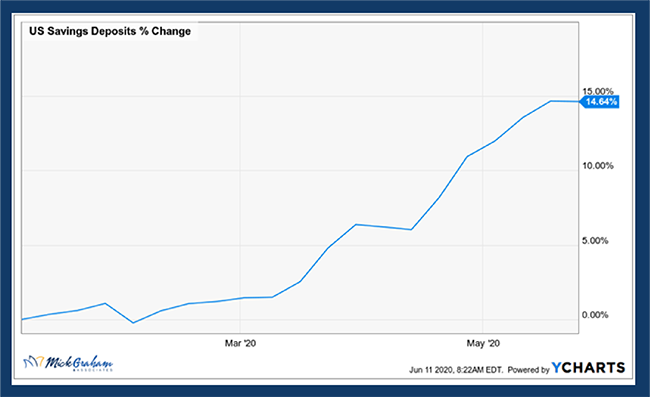

These moves have left me shaking my head…or as the kids say, SMH. I’m still in the camp of down too quick, back up too quick. Stimulus has given us some short-term reprieve on the statistics that can usually telegraph economic warning signs. The U.S. Savings rate is up 15% YTD and is now over $11T showing that most of the stimulus dollars are being left in deposit accounts and not spent.

We are a consumer led economy, therefore a high savings rate, although good for the long term, is concerning for the short to intermediate time frame, and that is where the market plays. The markets job is to estimate what earnings will look like 6 months from now. I’d also argue that the market struggles to look much more than 24 months in the future, meaning things that have potential to impact the markets long term (24 months or longer), don’t get priced in until they are in that zone.

Aside from the cyclicals leading early last week, the small caps (companies with a market cap of $1B and below) started to turn, along with the Equal Weighted index. The major indexes like the Dow and S&P 500 are market weighted indexes, meaning the bigger the company the more impact it has on the index. The equal weight index gives every company in that index the same percentage. The movement in small caps is relevant as they are the companies that potentially have the best growth opportunities and is the true sign that we have a strong economy. Small cap companies in economic declines often struggle to get the financing they need to sustain their growth plans (financing factories, investing in R&D etc). The banks in tough times would prefer to lend to the more stable names.

However, the Treasury’s stimulus plans have provided loans and, in some instances, “grant” to small business, providing the capital that they need to continue to innovate and grow. So why haven’t they contributed as much as the large caps is the true question. I think the answer to this is the same answer you will find in the question “why is the U.S. 10-year treasury still struggling to get off the low level since the start of this pandemic?” We saw a brief move higher last week, however that soon came back on Thursday.

There will be a winner and a loser in this scenario. This market has run so far so fast in the past month, while the treasury yield has not moved. I say the bond market is telling us something longer term, and the equities are looking at the re-opening and better employment numbers in the short term. Time will tell who wins, but as always, I’m listening to the wise old bond market.

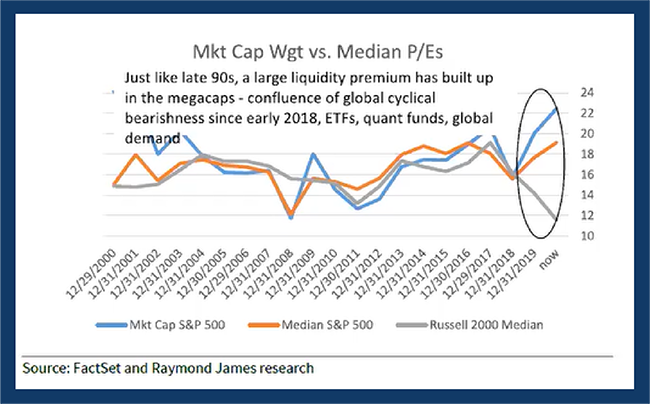

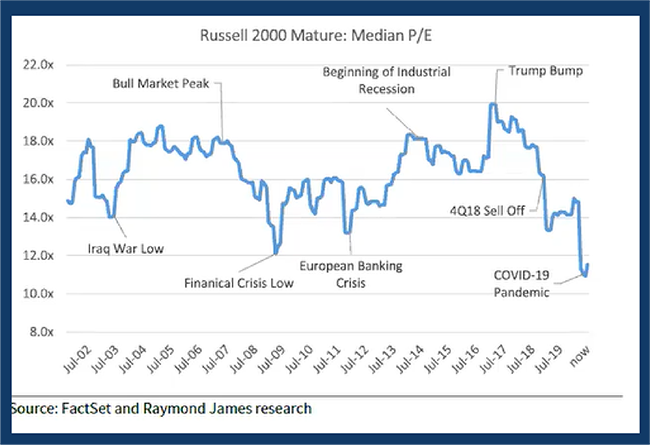

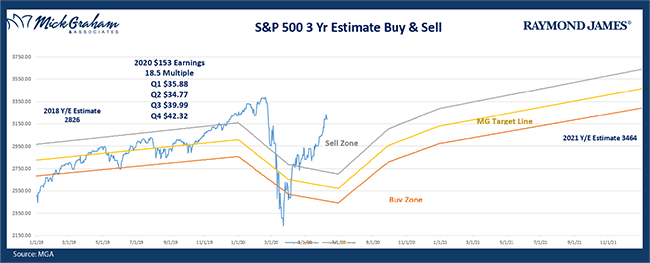

Below are a couple more charts of interest that I will go into more detail on the video.

With that here’s the buy/sell. Have a great week.

Any opinions are those of Mick Graham and not necessarily those of RJFS or Raymond James. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance may not be indicative of future results. Sector investments are companies engaged in business related to a specific sector. There are additional risks associated with investing in an individual sector, including limited diversification. Investing in small cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index.