This Week In Review: 6/10/2024

“If you put the federal government in charge of the Sahara Desert, in 5 years there’d be a shortage of sand.” - Milton Friedman

Good Morning ,

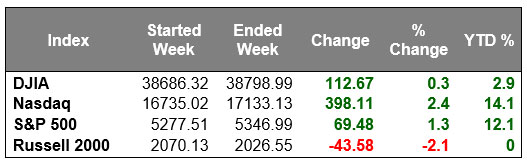

After the previous week’s sell-off, the broad indices reversed course last week.

Big tech rallied, bringing both the S&P 500 and Nasdaq into new all-time-high territory, with the Dow 30 trailing but still posting a positive return for last week. Markets also reacted positively to a strong jobs number in the U.S. and rate cuts from the Bank of Canada and European Central Bank.

The major indices logged gains last week largely thanks to mega cap stocks outperforming their smaller peers.

May’s positive momentum is carrying into June as both the S&P and Nasdaq have posted positive returns six out of the last seven weeks.

Big tech, including companies like Nvidia, is pushing the markets higher. Nvidia even surpassed $3 trillion in market capitalization, putting it roughly in line with Apple as the second and third most valuable company in the world behind Microsoft. The equal-weighted S&P 500 declined 0.7% versus a 1.3% gain in the market-cap weighted index. Still, the broader market showed nice resilience to any selling efforts.

The S&P 500 and Nasdaq Composite each logged a fresh all-time high last week. NVIDIA was the standout (again), topping a $3 trillion market value on a closing basis for the first time ever last week.

The strength in semiconductor stocks and mega caps boosted the S&P 500 information technology (+3.8%), consumer discretionary (+1.5%), and communication services (+1.7%) sectors to solid gains last week. Meanwhile, the utilities (-3.9%) and energy (-3.5%) sectors logged the largest declines.

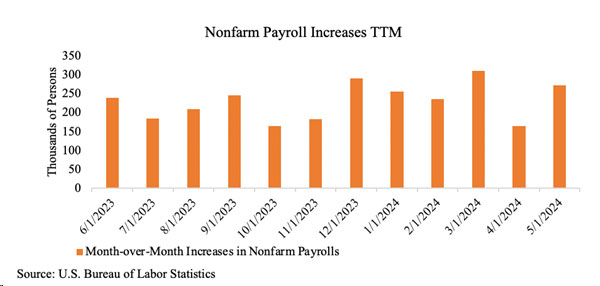

Nonfarm payrolls increased by 272,000 in the month of May, exceeding 185,000 jobs forecast by economists in a recent Reuters poll. The jobs report also stated hourly wages increased 0.4% while the unemployment rate increased to 4.0%.

This was another solid report showing a resilient U.S. labor market and likely pushed back expectations of a Fed rate cut in September.

While the unemployment rate did tick up to 4.0%, the highest since January 2022, year-over-year wage growth is 4.1%, giving employees “real” wages to spend. If wage growth is significantly above inflation, it gives households extra income to spend and save and in turn increases economic activity.

Concerns about economic growth kept the broader market in check in response to last week's economic data. The ISM Manufacturing Index for May reflected a faster pace of contraction than the market expected, job openings decreased in April compared to March, and the May Employment Situation Report showed higher than expected earnings growth.

Treasury yields settled lower in response to the data and in response to the first rate cut by the ECB since September 2019. The 10-yr note yield settled eight basis points lower this week to 4.43% and the 2-yr note yield declined two basis points to 4.87%.

Market Snapshot…

- Oil Prices – Oil prices finished with a third straight weekly loss on worries that demand may be softening. West Texas Intermediate crude was down three cents to $75.53 a barrel, while Brent crude futures were down 25 cents to $79.62 a barrel.

- Gold– Gold prices slid down 3% on the strong jobs report. Spot Gold dipped 3.69% to $2,305.96 per ounce. U.S. gold futures settled 2.8% lower to $2,325. Silver finished the week at $29.44.

- U.S. Dollar– The dollar rebounded after the economy reported a stronger job creation than expected. The dollar index rose 0.8% to 104.93; it’s best gain since April 10. Euro/US$ exchange rate is now 1.075.

- U.S. Treasury Rates– U.S. Treasury yields surged after May payrolls report topped expectations. The U.S. 10-year Treasury jumped nearly 15 basis points to 4.885%.

- Asian shares were mixed in overnight trading.

- European markets are trading lower.

- Domestic markets are trading higher this morning.

This week will focus on the Fed as it makes their next interest rate decision on June 12.

The overwhelming belief is that rates will be held steady at this meeting, but we will be watching for the new Summary of Economic Projections to see how the Fed believes the second half of the year will play out. The Fed has kept its benchmark interest rates at 5.25%-5.5% since last July.

March’s report indicated that the Fed was anticipating three rate cuts this year. Recent comments by Fed Members and economic reports, including May’s jobs report, all allude to this course of action being unlikely.

According to CME’s FedWatch Tool, the futures market has lowered its expectations and now foresees, at most, two cuts this year, one potentially in September and one more than likely in December. How inflation behaves over the next couple of months could determine the path for the remainder of the year.

Have a wonderful week!

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.