The Week in Review 12/04/23

"The big money is not in the buying or selling, but in the waiting. Spend each day trying to be a little wiser than when you wake up." – Charlie Munger

Good Morning,

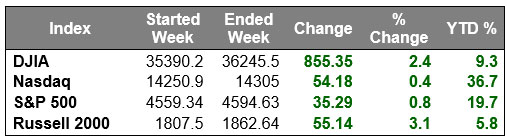

The stock market closed out the month of November with solid gains and began the month of December on a positive note.

Friday's close marked a new 52-week high for the S&P 500, which brushed up against the 4,600 level at its high of the day.

Only two of the S&P 500 sectors logged a decline, communication services (-2.5%) and energy (-0.1%). The rate-sensitive real estate sector (+4.6%) saw the biggest gain, followed by materials (+2.6%), industrials (+2.1%), and financials (+2.1%).

There was likely some fear of missing out on further gains in this seasonally strong period for the market contributing to the positive action this week, but the biggest driving factors were interest rates and rethinking rate cuts in the first half of 2024.

The 2-yr note yield, which is most sensitive to changes in the fed funds rate, plunged 39 basis points this week to 4.56%. The 10-yr note yield declined 24 basis points to 4.23%.

Also, the fed funds futures market now sees a much higher probability of a rate cut in May (89.0%) compared to one week ago (47.8%), according to the CME FedWatch Tool.

Some Fed officials pushed back on the idea that rate cuts will occur in the first half of 2024, but that did not deter investors. Richmond Fed President Barkin (2024 FOMC voter), Fed Governor Bowman (FOMC voter), and Fed Chair Powell all made comments last week indicating that they believe it is premature to talk rate cuts.

Investors received a slate of economic data last week that continue to look consistent with a soft-landing scenario for the economy.

Notable releases included: a stronger than expected November Consumer Confidence Index, an upward revision to Q3 real GDP to 5.2% from 4.9%, a moderation in income and spending, and disinflation in the PCE Price Indexes in October, a much stronger-than-expected Chicago PMI for November, and a relatively low level of initial jobless claims.

Market participants were also digesting more earnings news that was generally met with positive responses. Some of the most notable earnings news was the better-than-expected results from software enterprise names such as Snowflake and Elastic. Dow component Salesforce was another big winner after reporting earnings.

In other news, several OPEC+ countries confirmed additional voluntary cuts to the total of 2.2 million barrels per day, beginning January 1 through the end of March 2024. WTI crude oil futures declined 1.5% this week to $74.07/bbl.

Market Snapshot…

- Oil Prices – Oil prices continued sliding amid disappointing OPEC+ production cuts. West Texas Intermediate crude futures (WTI) fell $1.89, or 2.49% to close at $74.07 a barrel. Brent crude declined $1.98, or 2.45%, to close at $78.88 a barrel.

- Gold– Gold prices rose to an all-time high based on the Fed’s potential rate cuts. Spot Gold climbed 1.6% to $2,069.10 per ounce and rose about 1% last week. U.S. gold futures also settled 1.6% to $2,089.7. Silver finished the week at $25.857.

- S. Dollar– The dollar fell based on Chairman Powell’s cautious tone on further interest rate moves. The dollar index fell 0.2% and was at 103.23. Euro/US$ exchange rate is now 1.083.

- S. Treasury Rates– Treasury yields fell on Friday even though rate cut speculation is premature. The yield on the 10-year Treasury note fell more than 13 basis points to 4.213%.

- Asian shares were mixed in overnight trading.

- European markets are trading mostly lower.

- Domestic markets are mixed this morning.

More evidence of a resilient consumer came last week. According to Adobe Analytics, Black Friday shopping set a new online sales record of $9.8 billion, up 7.5% from 2022. Cyber Monday saw a 9.6% increase over 2022 to $12.4 billion. And total Cyber Week sales grew 7.8% to $38 billion. A slightly worrisome note in the data is the increase in buy now, pay later.

That payment method grew 42.5% year-over-year. What’s uncertain is if consumers are spending above their means for the holiday season, taking advantage of the discounts and seeking budgetary flexibility. In-store data is still forthcoming, but this initial look strikes a positive note for the holiday spending season.

Earnings are not bad…

With 98% of S&P 500 earnings results reported, the third quarter will mark the first quarter of year-over-year earnings growth since Q3 2022, up 4.8%. While most companies have reported, last week we heard from some prominent names in the software space.

As the calendar turns to December, we'll see if the market can continue its push higher in the form of a “Santa Claus” rally. A Santa Claus rally can occur toward the end of December and beginning of January. With the ongoing winning streak, we wouldn’t be surprised if a slight pullback occurred before Santa comes to town.

On the economic front, this week will feature November’s jobs report on Friday. Before that, we'll get October’s Durable Goods report on Monday, November’s PMI reports on Tuesday, and October’s Consumer Credit report on Thursday.

Have a wonderful week!

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.