Chief Economist Eugenio J. Alemán discusses current economic conditions.

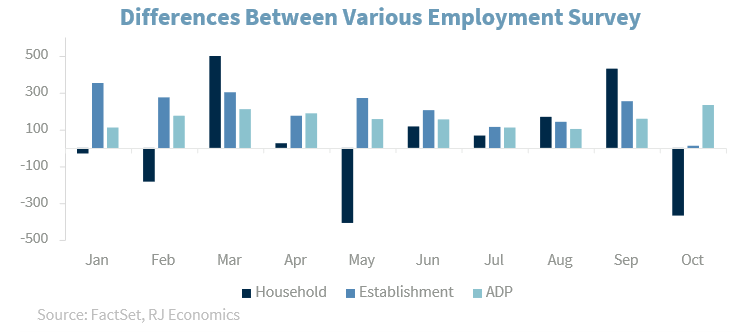

As you know, economists are normally criticized and accused of being ‘two-handed.’ This is because when we talk, we typically say, “on the one hand, and on the other hand.” Many argue that we are hedging our bets and lack the spine to take a position. While we disagree with that simplistic view of our job, we can understand why we are accused of being ‘two-handed.’ Well, today’s employment reports from the BLS and Wednesday’s report from the private payroll company ADP, have the potential to give rise to the existence of a ‘three-handed economist!!’

Why do we say this? Because the Establishment Survey, which we normally call the nonfarm payroll survey, indicated that employment in the U.S. was almost flat in October compared to September, only up by 12,000 new jobs. However, the Household Survey, which is the survey from which we calculate the rate of unemployment, showed that employment in the U.S. declined by 368,000 during the same month of October. However, to the amusement of conspiracy fearmongers, the rate of unemployment remained unchanged, at 4.1%, even with such a large loss of jobs! (See our employment indicator at the end of this document for why that was the case.) Furthermore, if you are not confused already, Wednesday’s ADP report, which is a survey done by the private payroll company ADP, indicated that employment in the U.S. increased by 233,000 in October. That is, on the one hand (+12,000), on the other hand (-368,000), and on the third hand (+233,000)!

Confused? Wait, there is more. Initial jobless claims, that is claims for unemployment insurance, which is a weekly figure, declined to 216,000 during the latest reported week, the lowest reading since April-May of 2024.

No wonder economics has been referred to as the ‘dismal science!’

But joke aside, the fact that these surveys are ‘different surveys,’ means they are conducted differently; are taken from different samples of the population, or different samples of businesses; and are taken at different times of the month, which has the potential to make the results different, especially when there are circumstances that could potentially distort the responses to these survey, as we had in October with the two hurricanes, the first one affecting Florida and the second one affecting Florida, Georgia, and North Carolina, plus the effects of the Boeing strike.

Thus, we would suggest those trying to understand all this information to ‘keep the eyes on the ball’ and take the employment information as just another data point (or 3 data points!) that allows us to help understand what is happening to the US economy. Today’s numbers don’t change what we have been saying about the labor market. That is, the labor market is slowing down but it is not tanking.

Going into next week, we will have to take a look at the October ISM Services PMI report on Tuesday to see if that Index shows a reversal in the strength shown in September. The reason for this is service sector employment was very weak in October, according to the nonfarm payroll number, and the ISM Services, and specifically, the Jobs component of that survey, may help confirm whether this was a one-off or if it is something that we should be more concerned with going forward.

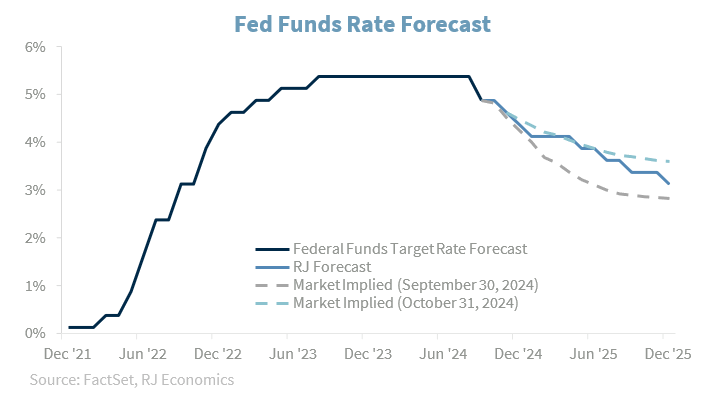

We also have the Federal Reserve (Fed) Federal Open Market Committee (FOMC) meeting decision on Thursday of next week and we are still expecting the Fed to cut the federal funds rate by 25 basis points.

The Federal Reserve’s job is not over: Markets are taking notice

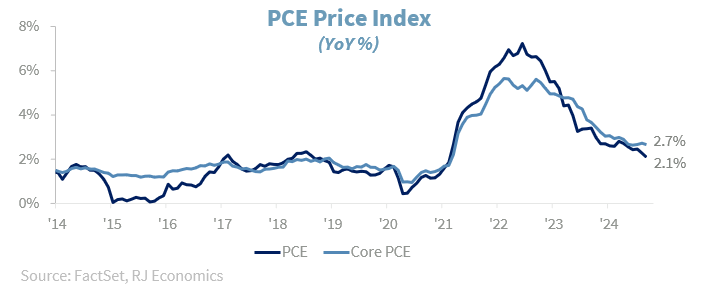

What the onslaught of economic data showed this week is not only that the Fed’s job is not over, but that it has become even more complex. At this point in time, Fed officials should be concerned about their ability to continue to lower inflation at a time when markets continue to pressure for more rate cuts. However, the data we have been getting does not support the Fed’s complacency. Although the disruptions from the COVID pandemic have dissipated almost completely, the Fed has to deal with a still strong economy that is not allowing the core PCE price index to continue to come down. While the Fed’s preferred measure of inflation, the headline PCE price index, hit 2.1% in September, year-over- year, the core PCE price index remained stubbornly high, at 2.7% for the third consecutive month. And this is not good for Fed policymakers and for the future path of interest rates.

Perhaps this is what has been internalized by the fixed income markets where the 10-year Treasury yield has moved considerably higher over the last month while the federal funds rate betting markets have also been pricing in fewer rate cuts for next year than they were after the September FOMC meeting.

As we argued during the week, we may see some increased hawkishness from Fed officials during the next several months. The Fed needs to slow down economic activity and while it argued in September that “rates had become too restrictive” the evidence since the September meeting does not conform with such a statement. Today’s employment numbers may indeed help convince the Fed and markets, that the economy has started to slow down. However, the Fed’s, interpretation of the data may not be as ‘plain vanilla’ as some may argue.

Barring any external shock that could put further pressure on oil and gasoline prices over the next several quarters, we will see the headline PCE price index probably dropping below the 2.0% target for several months. But the path for the core PCE price index is more uncertain than for the headline PCE price index and Fed officials are probably taking note, just as markets have, over the last several months, of the stickiness of the core PCE price index. Furthermore, the results of next week’s elections will also have important implications on monetary policy going forward. Thus, we will be attentive to all these variables and keep our readers informed on the potential path for rates.

But the Fed cannot ‘wish’ for something to not happen, it needs to pre-empt any potential spike in inflation by keeping the monetary spigot under control. That is, it needs to be aware that much lower interest rates could create an environment that can threaten the disinflationary process if there is a risk of much higher oil and gasoline prices.

Therefore, the Fed may be inclined to lower rates more slowly than earlier anticipated, especially if the economy continues to grow at current rates.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Last performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Statistics. Currencies investing is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation. Current Situation Index (CSI) and Future Expectations Index (FEI) are the end-results of CCI, covering economic conditions, employment, price, income, and expense. The reading is 100 plus the average of said five factors

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board's initial and ongoing certification requirements.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

GDP Price Index: A measure of inflation in the prices of goods and services produced in the United States. The gross domestic product price index includes the prices of U.S. goods and services exported to other countries. The prices that Americans pay for imports aren't part of this index.

The Conference Board Leading Economic Index: Intended to forecast future economic activity, it is calculated from the values of ten key variables.

The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The Index goes up when the U.S. dollar gains "strength" when compared to other currencies.

The FHFA House Price Index (FHFA HPI®) is a comprehensive collection of public, freely available house price indexes that measure changes in single-family home values based on data from all 50 states and over 400 American cities that extend back to the mid-1970s.

The Pending Home Sales Index (PHSI) tracks home sales in which a contract has been signed but the sale has not yet closed.

Supplier Deliveries Index: The suppliers' delivery times index from IHS Markit's PMI business surveys captures the extent of supply chain delays in an economy, which in turn acts as a useful barometer of capacity constraints.

Backlog of Orders Index: The Backlog of Orders Index represents the share of orders that businesses have received but have yet to start or finish. An increasing index value usually indicates growth in business but shows that output is below its maximum potential.

Import Price Index: The import price index measure price changes in goods or services purchased from abroad by

U.S. residents (imports) and sold to foreign buyers (exports). The indexes are updated once a month by the Bureau of Labor Statistics (BLS) International Price Program (IPP).

ISM Services PMI Index: The Institute of Supply Management (ISM) Non-Manufacturing Purchasing Managers' Index (PMI) (also known as the ISM Services PMI) report on Business, a composite index is calculated as an indicator of the overall economic condition for the non-manufacturing sector.

Consumer Price Index (CPI) A consumer price index is a price index, the price of a weighted average market basket of consumer goods and services purchased by households.

Producer Price Index: A producer price index (PPI) is a price index that measures the average changes in prices received by domestic producers for their output.

Industrial production: Industrial production is a measure of output of the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities. Although these sectors contribute only a small portion of gross domestic product, they are highly sensitive to interest rates and consumer demand.

The NAHB/Wells Fargo Housing Opportunity Index (HOI) for a given area is defined as the share of homes sold in that area that would have been affordable to a family earning the local median income, based on standard mortgage underwriting criteria.

Conference Board Coincident Economic Index: The Composite Index of Coincident Indicators is an index published by the Conference Board that provides a broad-based measurement of current economic conditions, helping economists, investors, and public policymakers to determine which phase of the business cycle the economy is currently experiencing.

Conference Board Lagging Economic Index: The Composite Index of Lagging Indicators is an index published monthly by the Conference Board, used to confirm and assess the direction of the economy's movements over recent months.

New Export Index: The PMI new export orders index allows us to track international demand for a country's goods and services on a timely, monthly, basis.

Durable Goods: Durable goods orders reflect new orders placed with domestic manufacturers for delivery of long- lasting manufactured goods (durable goods) in the near term or future.

Source: FactSet, data as of 9/20/2024