Chief Economist Eugenio J. Alemán discusses current economic conditions.

We have started to hear that inflation is no longer top of mind for US consumers and businesses going into 2025. Americans remain concerned with the level of prices, that is, with the fact that prices today are much higher than before the pandemic recession and this is one of the reasons they remain sour on the U.S. economy. The fight against inflation was not easy. How do you beat inflation back into submission if Americans amassed the means, due to accumulated excess savings, and the will, due to the pandemic lockdowns, to go back and enjoy life after such a difficult period in our lives? Not to mention the disruption from supply chains as well as the distortions created by some of these supply chains. Case in point, at some time during the period, a used car was more expensive than a new car! Just think about this!!

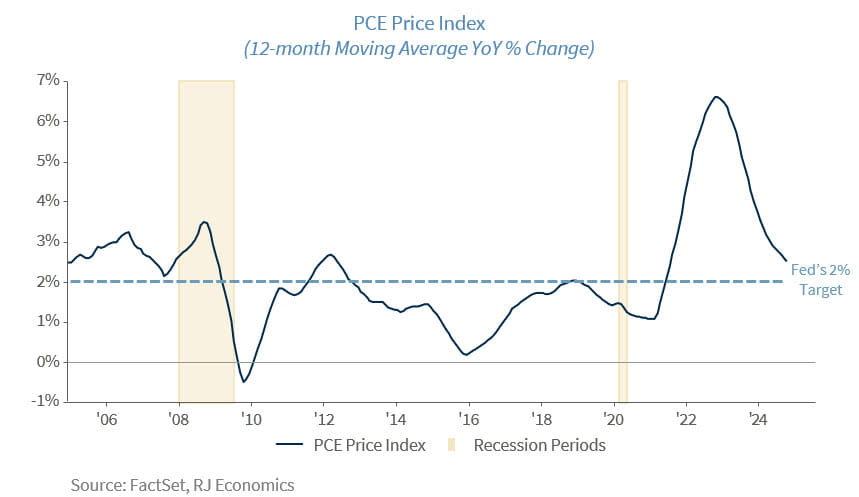

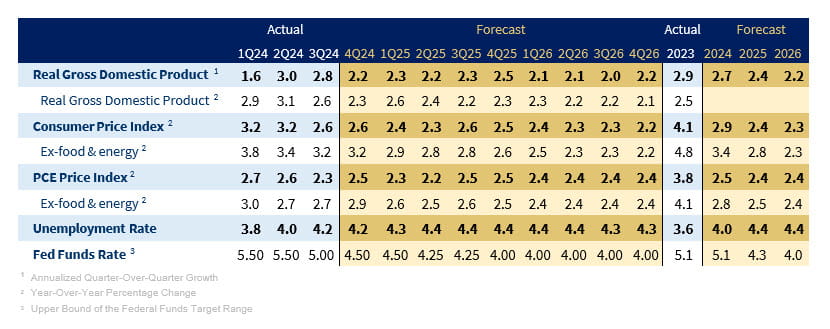

Today, the issues facing the Federal Reserve (Fed) are different. It has brought back the rate of change of prices, i.e., the rate of inflation, close to the coveted 2.0% target inflation rate. However, even though it seems that inflation is falling off the radar of Americans, it will be ever-present for Fed members during all of 2025. The incoming administration has proposed some policies that could keep the Fed on the defensive because the fight against inflation is still not over, as the “Federal Reserve seeks to achieve inflation at the rate of 2 percent over the longer run as measured by the annual change in the price index for personal consumption expenditures (PCE).”

That is, the fact that inflation is close to 2.0% is not good enough, the Fed needs to keep it at 2.0% over the longer run, not just for one or two months during a year. Furthermore, and for this we have to wait and see what the actual policies from the incoming Trump administration are going to look like, the potential for higher inflation down the road has increased due to some of the economic proposals, but especially by the potential imposition of a blanket tariff on all our trading partners. We understand that what ends up happening may be very different from what we have heard from President-elect Trump himself on these policies, but the Fed knows that anything that can disrupt inflation expectations in the future could be a threat to monetary policy and to the achievement of its inflation target.

On top of this, the proposal to deport illegal workers could also put more pressure on the rate of unemployment and we know that there is an inverse relationship between the rate of unemployment and the rate of inflation. That is, if the rate of unemployment is too low, the rate of inflation tends to go up. Today the U.S. economy has a very low unemployment rate compared to historical standards, allowing workers to push for higher salaries and wages. Thus, deporting an estimated 12 million illegal workers could put further downward pressure on the rate of unemployment and generate higher inflation through a wage-price spiral.

These are some of the reasons we believe that the Fed will be very careful with its interest rate policy going forward. We still believe that the Fed is going to lower interest rates during the December meeting of the Federal Open Market Committee (FOMC); however, our expectations for next year may soon align more closely with what markets are expecting today.

The U.S. labor market is alive and well

Although the two different employment surveys, the establishment and the household surveys released today showed a very different picture of the U.S. labor market in November, our overall view continues to be the same: the U.S. labor market is slowing down but it is not falling off a cliff (See our employment indicator below). The strong increase in service sector jobs in November compared to the slowdown reported in October is an indication that October’s numbers may have been an exception. At the same time, the change in employment in different sectors of the economy is also showing that in November, the U.S. consumer continued to be engaged in traveling and leisure activities while the recession-proof Health Care sector continued to drive employment growth during the month.

ISM Manufacturing: The November ISM Manufacturing PMI was higher than FactSet expectations, at 48.4 compared to expectations of a 47.5 reading, remaining in contraction territory for the eighth consecutive month after briefly reaching expansion territory in March. Today’s report showed overall little weakness except in the Prices Index, which is good news for the Federal Reserve (Fed) and inflation even though raw materials and petroleum prices helped the decline. On the other hand, New Orders increased and entered expansion territory for the first time since March, suggesting that demand ahead might accelerate. Inventories bounced back after two weak readings in October and September and returned near expansion territory, which is a level more consistent with a positive outlook. Lastly, despite remaining in contraction territory, Employment experienced a large increase during the month, which could be good news as we head into Friday’s Employment Report. According to the Institute for Supply Management, the ISM Manufacturing PMI remained in contraction territory, increasing from 46.5 in October to 48.4 in November. The New Orders Index increased from 47.1 in October to 50.4 in November. The Production Index increased from 46.2 in October to 46.8 in November. Inventories bounced back from 42.6 in October to 48.1 in November. Prices declined from 54.8 in October to 50.3 in November. New Export Orders increased from 45.5 in October to 48.7 In November. Employment also increased during the month, moving from 44.4 in October to 48.1 in November. The ISM Manufacturing Index improved more than expected in November but remained in contraction. The Prices Index decreased the most, while the Employment Index increased significantly, which is welcome news for the Fed as it gets ready to meet in two weeks for the last time in 2024.

Construction Spending: Total construction spending was higher than FactSet expectations for a flat month in October as residential construction spending was very strong during the month. This report seems to be at odds with the October housing starts report released several days ago, which showed a large decline in housing starts during the same month. However, the number on residential construction includes “private residential improvements,” which are not part of the housing starts report. Thus, it seems that this component of private housing construction spending was the driving force during the month of October. Total construction spending was up by 0.4% in October compared to September, at a seasonally adjusted annual rate of $2,174.0 billion. Compared to a year earlier, total construction spending was up by 5.0%, according to the US Census Bureau. Private construction drove the increase in October, according to the release, increasing by 0.7% compared to September of this year. There was a strong, 1.5%, month-on-month increase in residential construction during the month while nonresidential construction declined by 0.3% during the same period. Within private residential construction spending, new single-family construction spending was up by 0.8% while multifamily construction spending was up by 0.2%. Public construction was down by 0.5% in October of this year compared to September. The decline in public construction spending was due to a 0.4% decrease in educational construction spending as well as a 0.7% decline in highway construction spending. Within private nonresidential construction spending, manufacturing construction spending remained flat in October compared to September but is still up by 16.3% versus a year earlier. This component of private construction spending has slowed considerably but is still growing on a year-earlier basis due to the industrial policies supported by the CHIPS and IRA acts.

JOLTS: Job openings in October increased from a downwardly revised number in September. The largest drivers of the increase were Professional and Business Services (+209,000) and Leisure and Hospitality (+129,000). Today’s report is yet another indication that labor demand is softening but not collapsing, which is consistent with our view of a slowing economy and job market. Job openings increased to 7.7 million in October and were 941,000 lower than 12 months ago, according to the Bureau of Labor Statistics. FactSet expectations were for job openings to decline to 7.4 million. Hires were 5.3 million in October, the hires rate was 3.3%, and total separations were 5.3 million or 3.3%. On the other hand, quits increased to 3.3 million, pushing the quit rate higher to 2.1%. Job openings were revised down in September by 71,000, the number of hires was revised up by 24,000 and separations were unchanged.

ISM Services: After very strong performances by the service side of the US economy in September and October, the ISM Services PMI returned to the levels prevalent during the first half of the year. This means that the services sector has remained in expansion, but the strength of the expansion is showing signs of weakening. As the US economy approaches the end of the year it will be important to check inventory levels as well as imports, particularly given the possibility of tariffs as the new administration comes in. Since imports are a subtraction to economic growth, any non-typical movement by firms to upfront imports to avoid some of the higher costs of tariffs could have an impact on economic growth. For now, we believe that the slowdown in the service side of the economy is related to US consumers pausing their expenditures to prepare for the holiday season. The ISM Services PMI was lower than expected in November, at 52.1, compared to expectations for a 55.0 reading and much lower than the 56.0 reading in October. The Business Activity/Production Index came down from a strong 57.2 print in October to a still expansionary print of 53.7 in November while the New Orders Index was also down, from a strong 57.4 in October to a 53.7 print in November. The Employment Index was also lower but still expanding in November, as it came down from 53.0 in October to a reading of 51.5 in November. The largest declines occurred in the Supplier Deliveries and Inventories Indices, both of which went from expansion in October to contraction in November. The Supplier Deliveries Index declined from 56.4 in October to 49.5 in November while the Inventories Index decreased from 57.2 in October to 45.9 in November. The Prices Index moved slightly higher, from a reading of 58.1 in October to a reading of 58.2 in November while the Backlog of Orders Index declined from 47.7 in October to 47.1 in November. The New Export Orders went from expansion, at 51.7 in November, to contraction in October, at 49.6. The Imports Index was stronger in expansion territory, up from 50.2 in October to 53.8 in November while the Inventory Sentiment Index improved from 53.0 in October to 54.6 in November. The large decline in the Inventory Index was probably due to the strong performance of the service sector during October, as it showed inventories contracting compared to growing in the previous month. This is probably related to the relatively strong increase in the Imports Index, as many firms probably increased imports in order to replenish inventories.

Trade Balance: The lower trade balance in the goods and services deficit in October followed a very high deficit in the previous month that was triggered by the port strike. As firms tried to front end imports expecting disruptions from port closures the deficit skyrocketed in September while it came back down after the strike ended almost a week after it started. If firms see the potential for tariff implementation next year, we could see some similar effects at the end of this year and into next. In any case, this large reduction in the overall deficit is positive for economic growth during the last quarter of the year. The US trade deficit in goods and services was $10 billion lower than the September deficit, at $73.8 billion, according to the US Census Bureau and the Bureau of Economic Analysis. Exports were $265.7 billion in October, or $4.3 billion lower than in September while imports were $339.6 billion, or $14.3 billion lower than in September. On a Census basis, exports of goods declined by $5.3 billion as capital goods exports declined by $3.9 billion. Automotive vehicle, parts, and engines exports declined by $2.7 billion while exports of industrial supplies and materials declined by $2.5 billion. Exports of consumer goods declined by $1.3 billion while exports of other goods increased by $5.7 billion, according to the release. Imports of goods on a Census basis declined by $15.7 billion as capital goods imports declined by $7.5 billion. Industrial supplies and materials declined by $3.3 billion while consumer goods imports declined by $2.0 billion. Finally, imports of automotive vehicles, parts, and engines declined by $1.6 billion. Trade data during the last several months has been affected by the US port strike as firms increased imports considerably ahead of the strike and now imports have corrected downwards again.

Employment Report: Employment, as measured by the nonfarm payroll survey increased strongly in November after an upwardly revised number for October while the unemployment rate increased slightly. Once again, both employment surveys disagreed with the stance of the US labor market in November. The strong recovery in job creation in the leisure and hospitality sector showed that November was a very good month for traveling while the decline in retail trade jobs is pointing to a not so good month for retail sales. What this report showed is that the US labor market has continued to weaken but it is not falling apart, which is in line with our views on the US economy. Nonfarm payrolls for November came out at 227,000, stronger than the FactSet expectation for an increase of 200,000 while the original print for October of just 12,000 new jobs was revised higher to 36,000, according to the Bureau of Labor Statistics. The total revision for the previous two months was positive by 56,000. The rate of unemployment moved slightly higher, from 4.1% in October to 4.2% in November. Total private employment increased by 194,000 in November after falling by an upwardly revised 2,000 jobs in October. The goods-producing sector created 34,000 jobs during the month after eliminating 44,000 in October, mostly due to the strike at Boeing. Overall, manufacturing jobs increased by 22,000 during the month after falling by 48,000 in October. The construction sector added 10,000 jobs during the month after adding just 2,000 during the previous month. Jobs in the private service-providing sector recovered strongly during November, creating 160,000 jobs after slowing down to 42,000 in October. Jobs in the retail trade sector were very weak, shedding 28,000 positions in November while jobs in financial activities increased by 17,000 during the month. The professional and business services sector added 26,000 jobs during the month after shedding 23,000 jobs during the previous month. The private education and health services sector added 79,000 jobs during the month, with most of them created within the health care and social assistance sector, up 72,300. Finally, the leisure and hospitality sector added 53,000 jobs during the month after adding just 2,000 jobs in October. The government sector added another 33,000 jobs in November after adding 38,000 jobs in October. Average weekly hours increased slightly, from 34.2 in October, to 34.3 in November while average hourly earnings increased from $35.48 to $35.61. Thus, average weekly earnings increased from $1,213.42 in October to $1,221.42 in November. Once again, the Household survey showed a very different picture of the US employment market. Employment in this survey declined by 355,000 during November while the civilian labor force declined by 193,000. Thus, the labor force participation rate decreased from 62.6% in October to 62.5% in November.

Consumer Sentiment: Consumer sentiment was higher than expected in December, according to the University of Michigan Survey of Consumers. Current Economic Conditions jumped 13.8 points, the largest one month change since November 1992, to the highest level since April, while the Expectation Index declined to the lowest level since July. We believe these large fluctuations will stabilize and are likely exacerbated by the outcome of the election. Meanwhile, inflation expectations were also mixed, with one year-ahead inflation expectations increasing but longer-term inflation expectations declining. The University of Michigan's preliminary Consumer Sentiment Index for December increased from 71.8 in November to 74.0 in December, according to the release. However, the subcomponents of the Index were mixed. The Current Economic Conditions Index increased significantly, from 63.9 in November to 77.7 in December while the Index of Consumer Expectations experienced a large decline from 76.9 in November to 71.6 in December. One year-ahead inflation expectations increased to 2.9% in December compared to a reading of 2.6% in November. However, longer-term inflation expectations, the five years-ahead index, decreased from 3.2 in November to 3.1% in December, preliminarily.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Statistics. Currencies investing is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation. A value above 100 signals a boost in the consumers’ confidence towards the future economic situation, as a consequence of which they are less prone to save, and more inclined to consume. The opposite applies to values under 100.

Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States to Certified Financial Planner Board of Standards, Inc., which authorizes individuals who successfully complete the organization’s initial and ongoing certification requirements to use the certification marks.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

GDP Price Index: A measure of inflation in the prices of goods and services produced in the United States. The gross domestic product price index includes the prices of U.S. goods and services exported to other countries. The prices that Americans pay for imports aren't part of this index.

Employment cost Index: The Employment Cost Index (ECI) measures the change in the hourly labor cost to employers over time. The ECI uses a fixed “basket” of labor to produce a pure cost change, free from the effects of workers moving between occupations and industries and includes both the cost of wages and salaries and the cost of benefits.

US Dollar Index: The US Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The Index goes up when the

U.S. dollar gains "strength" when compared to other currencies.

Import Price Index: The import price index measure price changes in goods or services purchased from abroad by U.S. residents (imports) and sold to foreign buyers (exports). The indexes are updated once a month by the Bureau of Labor Statistics (BLS) International Price Program (IPP).

ISM Services PMI Index: The Institute of Supply Management (ISM) Non-Manufacturing Purchasing Managers' Index (PMI) (also known as the ISM Services PMI) report on Business, a composite index is calculated as an indicator of the overall economic condition for the non-manufacturing sector.

Consumer Price Index (CPI) A consumer price index is a price index, the price of a weighted average market basket of consumer goods and services purchased by households.

Producer Price Index: A producer price index(PPI) is a price index that measures the average changes in prices received by domestic producers for their output.

Industrial production: Industrial production is a measure of output of the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities. Although these sectors contribute only a small portion of gross domestic product, they are highly sensitive to interest rates and consumer demand.

The NAHB/Wells Fargo Housing Opportunity Index (HOI) for a given area is defined as the share of homes sold in that area that would have been affordable to a family earning the local median income, based on standard mortgage underwriting criteria.

Conference Board Coincident Economic Index: The Composite Index of Coincident Indicators is an index published by the Conference Board that provides a broad-based measurement of current economic conditions, helping economists, investors, and public policymakers to determine which phase of the business cycle the economy is currently experiencing.

Conference Board Lagging Economic Index: The Composite Index of Lagging Indicators is an index published monthly by the Conference Board, used to confirm and assess the direction of the economy's movements over recent months.

New Export Index: The PMI New export orders index allows us to track international demand for a country's goods and services on a timely, monthly, basis.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The Conference Board Leading Economic Index: Intended to forecast future economic activity, it is calculated from the values of ten key variables.

Source: FactSet, data as of 12/6/2024