Beneath The Surface

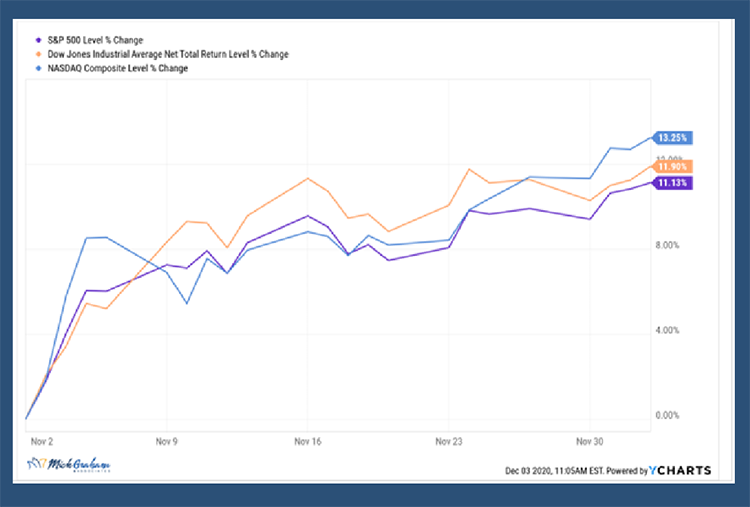

Just looking at the major indexes (S&P 500, Dow Jones Industrial Average & Nasdaq), you look and say the market is on a tear. The one month returns for all three of the indexes are double digits. However, looking beneath the surface tells you a different story.

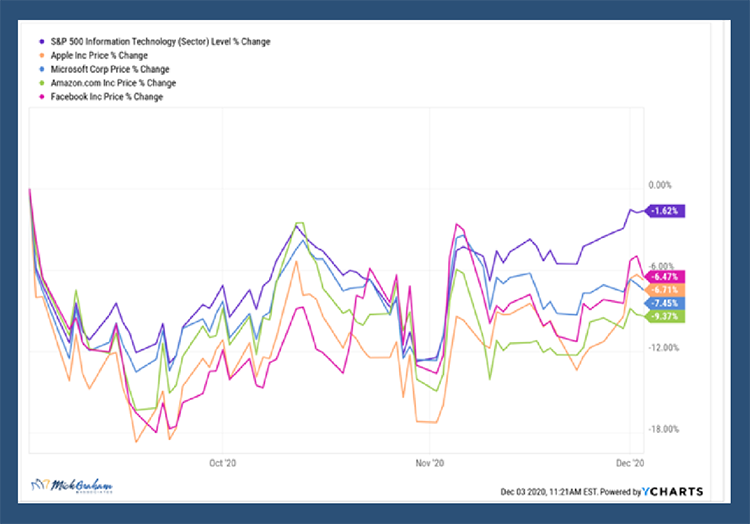

This market recovery from March (and for that matter the past three years), can be credited to the largest components of the index. A quick Google search will tell you who the biggest 5 stocks in the indexes are. This past month however, only one of the big 4 stocks made double digit returns. So, who can we credit for the latest moves? The small and mid-caps.

Remember, due to the indexes being market weighted, it takes a lot more for a small company to move the overall index than the larger companies. The big boys get a bigger weighting and therefore they have the ability to affect the index.

So why am I telling you the same thing I told you last week, (and the week prior)? Because I believe this is the changing of the guard. The easy money went to the big safe names over the past few years and particularly in the past 8 months, but those times I think are over. I just want to prepare you to look beyond what the TV is saying and monitor your account instead.

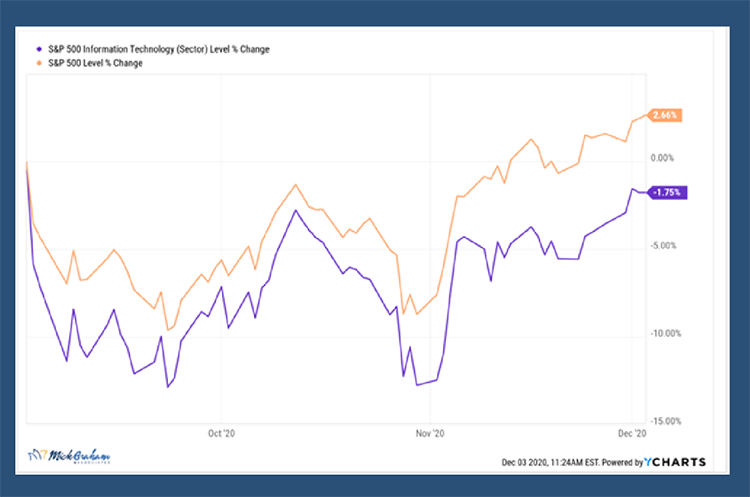

If I change the graph to go back to September 2nd, I can tell you that the S&P 500 Tech sector was negative 1.2%, and the big four names of the index were down between 6.47% and 9.37% during that time.

What this tells me is that if the major players in the index were down, but the overall index is higher, there must be a heck of a lot of other names that are contributing to the overall index return, and this is exactly what happened. Last week we had around 90% of the names in the S&P 500 above their 10-day moving average. Not the highest it’s ever been, but right up there. As I write today, that has pulled back to just under 70%, but still shows a breadth of solid support for the market as a whole.

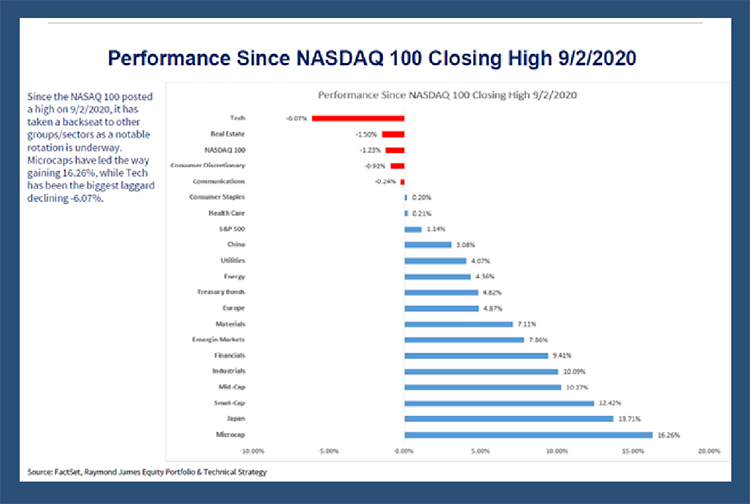

My days now are under the hood looking for pockets of opportunity, especially on days when we get more than a 1% move in the indexes. You can see from the chart above, the massive moves are not only between the size and style of the market, but the sectors as well. The one stat that I feel is very telling is although we have markets at all-time highs, there is still around 20% of the components of the index that are still over 15% negative for the year. This is exactly where I believe the opportunity lies.

Short-term, however I do think we could pull back or stay steady for a while. Although not completely overbought, we are on the higher side as the market is looking for the next stimulus package before this congress recesses or packs their bags for good. Longer term, I’m a bull. Too much stimulus, too low of rates, 20% + earnings growth next year and TINA (There is no alternative).

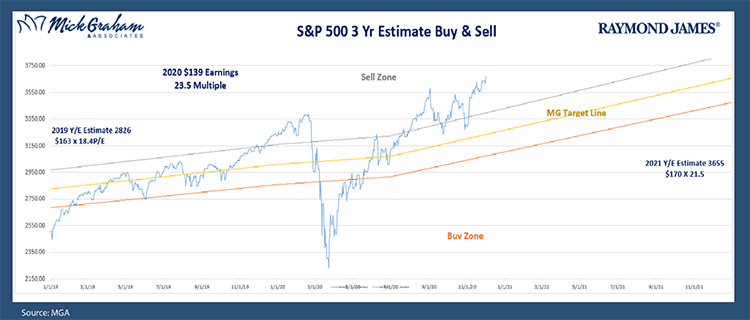

With that here’s the buy/sell.

Any opinions are those of Mick Graham and not necessarily those of RJFS or Raymond James. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Sector investments are companies engaged in business related to a specific sector. The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Inclusion of these indexes is for illustrative purposes only. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal. The NASDAQ-100 (^NDX) is a stock market index made up of 103 equity securities issued by 100 of the largest non-financial companies listed on the NASDAQ. It is a modified capitalization-weighted index. ... It is based on exchange, and it is not an index of U.S.-based companies. The NASDAQ composite is an unmanaged index of securities traded on the NASDAQ system. The S&P MidCap 400® provides investors with a benchmark for mid-sized companies. The index, which is distinct from the large-cap S&P 500®, measures the performance of mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment. The S&P 1500 is a stock market index of us stocks made by Standard & Poor's. It includes all stocks in the S&P 500, S&P 400, and S&P 600. This index covers 90% of the market capitalization of U.S. stocks.