By Daniel Staiger, CFP®, CRPC®

It’s common knowledge that Medicare plays a big role in the healthcare plans of numerous retirees across the United States. Initially introduced in 1965, Medicare generated a substantial revenue of $988 billion in 2022 while providing benefits to a staggering 65 million individuals. As of today, almost 96% of individuals aged 65 and older rely on Medicare.

Despite the pivotal role Medicare can play in supporting your financial future, many people lack a full understanding of the benefits available to them. Not knowing how the system operates and how those benefits can be positioned can potentially result in big financial consequences. If you’ve ever attempted to navigate the process of Medicare only to find yourself feeling overwhelmed and confused, you’re an ideal candidate for a Medicare evaluation.

Medicare is a health insurance program provided by the federal government for people over the age of 65 as well as disabled individuals. As mentioned, it plays a key role in covering healthcare costs in retirement, but it is not meant to cover everything. Understanding its coverage and its limitations is a crucial part of being prepared for retirement.

Medicare is divided into four parts: Part A, Part B, Part C, and Part D. There are also supplemental coverages to consider. Here is an overview of the different options to review as you approach retirement:

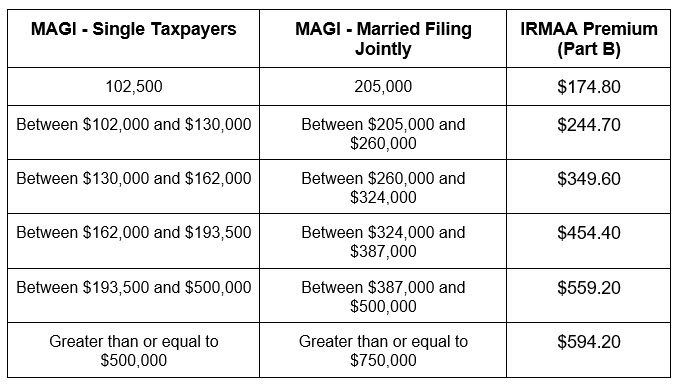

Keep in mind that basic Medicare does not cover long-term care, dental care, vision or hearing care. This includes Medigap supplemental coverage. You may think that you’re getting additional services when you enroll in Medigap, but that is not the case. Medigap only helps out with deductibles and copays, it will not provide additional services that Medicare does not cover. If these expenses are not properly planned for, it can be detrimental to your overall retirement plan.

What to expect depends on which stage of the Medicare process you’re in.

If you’re a pre-retiree thinking about enrollment, you should expect to sign up in the six months surrounding your 65th birthday (three months before and three months after). If you’re receiving Social Security benefits at that time, you will be automatically enrolled in Medicare Part A and Part B. Additional coverages like Part D, Medigap, and Medicare Advantage will have to be enrolled separately. If you’re not receiving Social Security when you turn 65, you will have to apply for Medicare through the Social Security Administration website.

If you’re retired and already enrolled in Medicare, you should expect to review your benefit options every year. This year, Medicare open enrollment began on October 15th and remains open through December 7th. The decisions you make during this period will affect your 2024 Medicare coverage. It’s a daunting task, but Medicare costs and coverage levels change annually so it’s important that you stay up to date.

If you are already enrolled in Medicare, here is what you can do with your Medicare coverage during the enrollment period:

Don’t get this confused with the Medicare Advantage open enrollment period that occurs from January 1st to March 31st, where those with Part C can change to a different Part C plan or switch to Parts A and B. Any other changes need to happen in the October-December enrollment period.

If you're feeling overwhelmed and your thoughts are in a whirlwind, you're in good company! The confusion you feel is a normal reaction when our clients sift through their Medicare options. That's precisely why we're here, ready to help clear the air.

At Matarazzo Staiger, we work with our clients to make sure they approach their Medicare plan decisions with confidence. Whether you're grappling with questions about your existing Medicare coverage or need guidance during the enrollment process, don't hesitate to get in touch with us today. Claim your complimentary appointment by contacting us at daniel.staiger@raymondjames.com or calling (631) 319-6777.

Daniel Staiger is a partner at Matarazzo Staiger Wealth Management and Financial Advisor with Raymond James Financial Services. Matarazzo Staiger Wealth Management is an Independent Practice and our team is committed to helping families, pre-retirees, and union employees build a sense of security and confidence around their financial future. With more than 10 years of experience, Daniel is dedicated to providing trusted advice and tailored solutions that help his clients realize their financial potential. He is known for building relationships with his clients so he can better understand their values and the goals they want to pursue. As a CERTIFIED FINANCIAL PLANNER™ and Chartered Retirement Planning Counselor℠ professional, Daniel specializes in serving union employees, such as tradespeople and teachers, with well-thought-out guidance and a personal touch. When he’s not working, Daniel spends his time pursuing interests such as guitar, volleyball, golf, and cooking. He is also an active member of his church. To learn more about Daniel, connect with him on LinkedIn.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board's initial and ongoing certification requirements.

Every investor's situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation.