Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Investors have much to be thankful for in 2024

- Economic resilience and positive EPS growth support returns

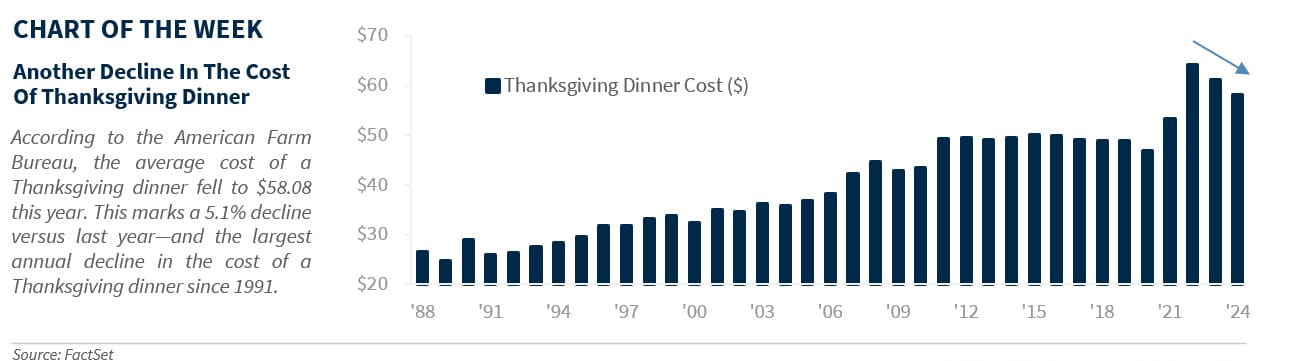

- The cost of Thanksgiving dinner declines for second straight year

Happy Early Thanksgiving! No Thanksgiving would be complete without giving thanks and expressing gratitude for all our colleagues, clients and loyal readers. On behalf of the Investment Strategy team, we wish you and your family a happy, healthy and hearty Thanksgiving. Whether you are home for the holiday, traveling to a domestic destination or are heading overseas for a new adventure (like so many others as international flight bookings are up 23% compared to last year), there are so many things to be thankful for this year. On a fun note, this Thanksgiving we are thankful to have another opportunity to enjoy Turkey and all the trimmings, Football and Good Old-Fashioned Apple Pie with our family and friends! And as we look through our financial lens and reflect upon everything that has transpired in 2024, we have compiled a list of the top ten economic and market-oriented things that we are most grateful for this year:

- US Economy Not Going Into A Recession—The macroeconomic stars were aligned in 2024, keeping economic growth near trend despite concerns that tight monetary policy would lead to a more pronounced downturn. A key factor behind the ongoing strength in the economy has been the remarkably resilient labor market—which produced nearly 2 million jobs this year.

- Disinflationary Trends Are Still Intact—Inflation remains on a path to gradually ease back to the Fed’s 2.0% target. While the last mile of the disinflationary process has been bumpy, there is plenty of evidence that suggests that the trend remains intact. A combination of well anchored inflation expectations, moderating wage pressures, lower commodities prices, retailers and restaurants increasing promotional activity and waning corporate pricing power—gives us good reason to think inflation will stay on the right track.

- Fed Easing Cycle Has Begun—After the most aggressive rate tightening cycle in 40 years and the second longest pause on record, the Fed finally kicked off its easing cycle in September as policymakers gained confidence that inflation was sustainably moving back to target and the economy was normalizing from post-pandemic distortions. The Fed’s decision to start dialing back its policy restraint should help prolong the expansion and keep the economy on a path to a soft-landing—the first soft-landing since 1995.

- Cash Provides An Attractive Yield—The historically low interest rates after the Great Financial Crisis punished savers. However, the silver lining of the post-pandemic bond market rout has been that interest rates have returned to more normal levels. That means that savers are no longer penalized for holding cash. And with the yields on cash alternatives and money markets near 4.5%, savers can now earn a respectable rate on assets that they need to keep liquid. It’s also been great for retirees.

- Retail Investors Are Big Buyers Of Treasuries—Market concerns about who was going to buy the ever-increasing amount of US debt have been unfounded. Yes, yields have normalized from their post-pandemic lows, but this is a good thing as ‘income’ is finally back in fixed income. Retail investors have enthusiastically stepped up to take advantage of the highest interest rates in more than 15 years as the Fed is no longer the main buyer of US Treasuries. And with interest rates still at attractive levels, demand should remain strong.

- Second Year Of 20+% Returns—The S&P 500 is on pace to rally 20% or more for the second consecutive year for the first time since the late 1990s. Rising equity prices have been a major contributor to consumer net worth, which is up 12% over the last two years to a new record high. Rising net worth has supported consumer spending—particularly for the higher-end consumer.

- Strong Earnings Growth—S&P 500 earnings are expected to rise 10% in 2024 and 15% in 2025. Robust earnings and cash flow have propelled buybacks (up 12% YoY in 3Q24) and dividend increases. Positive shareholder friendly actions should continue to support returns.

- AI Tailwinds—Spending on Artificial Intelligence has boosted the tech sector, which is on pace to outperform the S&P 500 by 10% for the second straight year. AI investment has also supported capex, as S&P 500 capex has increased for 3 straight quarters and is up 17% YoY.

- Oil Below $70—Record oil production in the US helped offset the upside risk from geopolitical unrest (Russia/Ukraine, Israel) overseas. Oil prices remaining below $70/bbl has helped to push gas prices down to $3/gallon, which is supportive of consumer spending.

- A Less Expensive Thanksgiving Meal—Thanks to disinflationary impacts, the cost of the Thanksgiving Dinner declined for the second consecutive year in 2024 and posted the largest annual decline (5.1%) since 1991. As rising grocery prices have been a key impediment for the consumer since 2021, easing prices will allow consumers to spend their money in other ways!

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.