Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

The elections have ended resulting with roughly half of you excited and the other half disappointed. That statement was sure to resonate regardless of the election results. What follows is the onslaught of calls inquiring about what strategic move needs to be made given the outcome.

Conjecture builds with the assumption that regulation constraint, antitrust enforcement, and business directive will all be loosened by the incoming administration. Government involvement and regulation likely will be much friendlier – at least domestically. Tariffs on imported goods might go up which could make items we buy more expensive. Tariffs are in essence a tax on goods as the cost is passed to the consumer. Could this reinflate prices or slow growth? So many questions, so many possibilities.

Instead of spending countless hours stressing about a perfect strategic move to capitalize on all the possible outcomes about to surface, let’s remember some of the more practical strategic views. The world is constantly changing and chasing the latest momentum swing may provide mixed results. We change presidents every four years, House of Representative members every two years, and senators every six years. The Chairman of the Federal Reserve is appointed every four years. Things and people are changing on an ongoing basis.

Your fixed income strategy does not necessarily need to be adjusted based on every personnel or environmental change. Long term strategic plans often weather the day-to-day or even year-to-year momentum swings. This is why we often look to the big picture and extended periods when attempting to optimize your goals.

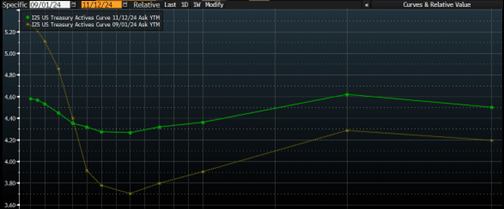

The market could see increased volatility as investors jockey on the latest economic data, personnel appointment, or geopolitical event. It is a mere 90-day lookback when the election appeared to be a coin toss. In that time-period, the yield curve has dramatically reshaped. I believe this direction (normal steepening) will likely continue to play out. Yields from 2 to 30 years are meaningfully higher. Short-term rates (<1 year) are appreciably lower. The yield curve has consequently flattened. As long as inflation remains steady or drops, the Fed is likely to continue to ease the Fed Funds rates. This is what impacts short rates the greatest. They have lowered this rate by 75 basis points over their last two Federal Open Market Committee meetings and have one remaining meeting this year in mid-December. Ultimately, I believe this will push the curve to a normal upward slope finally ending a historically long inverted Treasury curve which has provided higher 3-month T-Bill rates versus lower 10-year Treasury note rates.

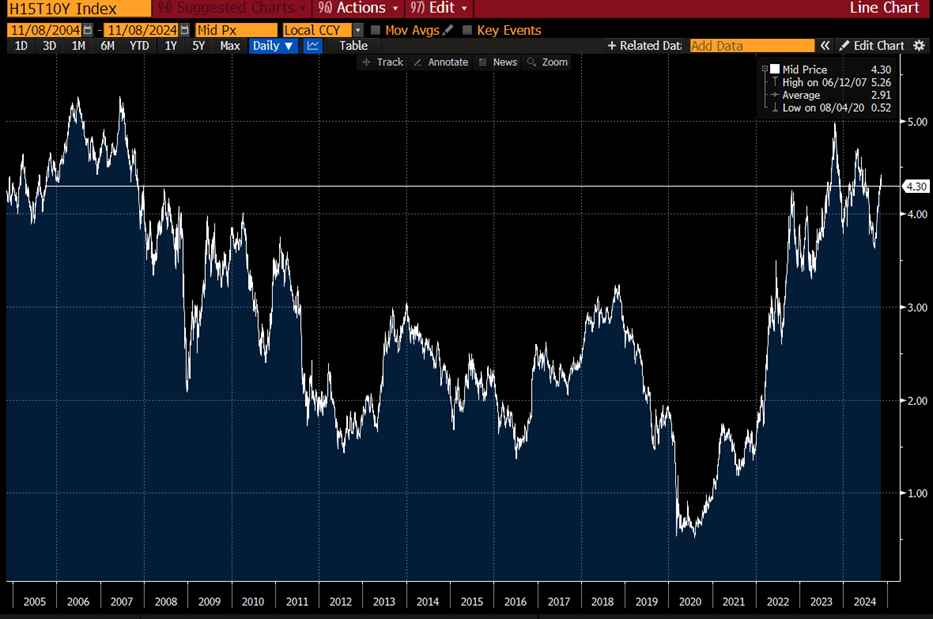

The long term strategy for fixed income remains intact. In order to address risks associated with fluctuating rates and changing yield curve shapes, laddered or bar belled investing mitigates the unknown without constantly changing or investing for or at the moment. Staggered maturities allow you to invest in all markets and not be subject to a specific investment date. As the Treasury curve returns to a normal upward slope, investments will once again provide additional reward for taking on additional interest rate risk associated with extending out in maturities. Given our generally high-interest rate environment, adding duration allows you to lock into these elevated rates for longer. The market continues to provide yields not seen in 17 years and although it is not at its peak, the general interest rate levels are relatively high. As the stock market continues to push portfolio growth at an accelerated pace, it may pay long term dividends to continue to balance the asset allocation by taking some of the growth and locking it into fixed rate assets.

Avoid the allure associated with at-the-moment events and trying to out-guess the volatile markets. Focus on the long term and take advantage of elevated interest rates by locking in for longer while mitigating risk through laddered and bar belled portfolio strategies.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.