Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- A soft landing should ensure the expansion enters a fifth year

- Despite slower job growth, the unemployment rate should stay low

- Solid earnings growth and a resilient economy should support U.S. equities

Happy Holidays! As the page for the new calendar year will soon turn, three cheers for a happy, healthy, and prosperous new year! With 2024 rapidly drawing to a close, we reflect on the year and all that’s transpired—our readers are wonderful, the economy remains in good shape, and market returns have been stellar for those who participate. However, the Fed’s final meeting of the year threw the markets a twist—with equity volatility spiking, U.S. equities struggling and yields heading higher as inflation uncertainty lurks. But with inflation expectations still anchored and S&P 500 earnings expected to move higher, any near-term setbacks in the financial markets should remain just a blip. The release of our Ten Themes for 2025 (i.e., specific asset class views with actionable investment ideas) is just a few weeks away, but we want to share our 12 aspirational wishes (i.e., high-level macro events) that, if they come true, should help the economy and markets prosper in 2025. They include:

- One Year Of World Peace | While tensions remain elevated across the globe—with ongoing wars in Europe and the Middle East and an upheaval in politics following the Global Election super-cycle in 2024—we are hopeful that 2025 will bring more stability and world peace. Our wish for a ceasefire to the conflicts that exist and less political discourse in the new year would surely be a wonderful gift.

- Inflation Moves Back To Two Percent | The Fed’s preferred measure of inflation (core PCE) has nearly halved (2.8%) from its peak, but progress has recently stalled above the Fed’s 2.0% target level. While inflation worries have intensified as growth remains resilient and tariff uncertainty is top of mind, here’s hoping the disinflationary trend resumes and progress toward 2.0% will not be doomed.

- Gas Under $3.00 A Gallon | With gas prices falling steadily since the mid-point of this year, consumers have had plenty of reason to cheer. With budgets still strained and consumers more discerning, gas below $3.00/gallon would bring some additional relief to their burden.

- Four Percent Unemployment Rate | The labor market has rebalanced from its post-pandemic strength, but despite a slowdown in hiring, layoffs remain reassuringly low. While the unemployment rate (4.2%) has ticked up from its historic low (3.5%)—a soft landing and Fed rate cuts should ensure the economy remains at full employment. A 4.0% unemployment rate would be something to celebrate.

- GDP Growth For Five Years In A Row | While the Fed’s aggressive tightening could have derailed growth in 2024, the economy proved more resilient than expected by policymakers and others. With a few timely rate cuts by the Fed and a surge in confidence following the election, the economy remains poised to continue its expansion. As we enter the new year, five years of GDP growth is likely to appear.

- Biggest Six Mega-Cap Tech (MAGMAN) Soar To New Heights | AI enthusiasm has been a big theme, driving equity prices to levels rarely seen! While valuations are lofty, earnings momentum and high margins are driving gains, our wish in 2025 is more of the same. Another year of mega-cap tech thriving would make 2025 a prosperous year for all.

- S&P Climbs To 7,000 | As the S&P 500 notched 57 record highs in 2024, the equity market has continued to soar. With the economy entering 2025 with strong momentum and plenty of potential catalysts (i.e., tax cuts, deregulation, improving sentiment) on the horizon that could take earnings to new heights, the S&P 500 touching 7,000 (our bull case) would certainly be a delight!

- $8 Trillion Debt Maturing Meets With Strong Treasury Demand | The market’s focus on the deficit and debt dynamics could give US Treasuries a scare, with yields heading higher as investors prepare. While demand has remained healthy overall, we hope that strong demand for upcoming maturities and new issuance continues in the new year, which would give the bond market something to cheer.

- Investment Grade Spreads (Under 0.9%) Remain Low | While investment grade spreads are hovering near historic lows, strong demand has continued as the macroeconomic backdrop still glows. With credit fundamentals (i.e., strong balance sheets, rising earnings, solid growth) still healthy and investors searching for attractive yields, we hope that credit spreads remain narrow throughout the new year.

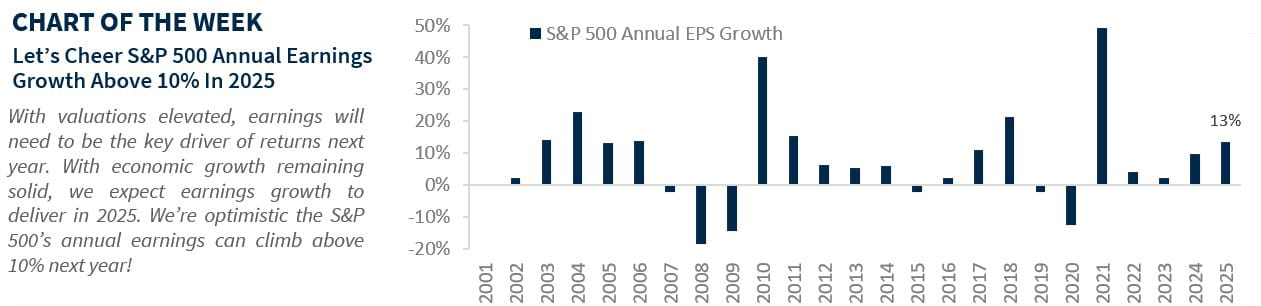

- S&P 500 Sees 10+% Earnings Growth | While S&P 500 2024 earnings growth was powered by mega-cap tech, strong growth and a broadening of earnings will be key in the year ahead. The third year of a bull market often brings muted gains, but if the S&P 500 can achieve 10% earnings growth in 2025, investors will toast with a glass of champagne!

- All Eleven Sectors In Positive Territory | Two consecutive years of 20+% performance sure has been great, as all eleven sectors of the S&P 500 have been able to participate. With optimism heading into 2025, we hope all eleven sectors continue to thrive!

- May 12 Doves Prevail Among The FOMC Members | While the Fed’s easing cycle has brought some dissents, we hope policymakers can get on the same page as inflation resumes its descent. We wish for 12 voting doves to appear, so rates can move lower in the new year.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.