This week in review: 1/13/25

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.” – Benjamin Graham

Good Morning ,

Markets continued their selling last week. A strong jobs report and hawkish Fed minutes caused stocks to sell off as investors lessened their expectations for further rate cuts in 2025.

Rising interest rates were a big driving factor in last week's action, reflecting worries about sticky inflation and that the Federal Reserve may maintain higher interest rates for an extended period.

The 10-yr yield surged 18 basis points last week to 4.78% and the 2-yr yield settled 12 basis points higher than last Friday to 4.40%. This price action was in response to last week's economic releases.

The reports include a stronger-than-expected ISM Services PMI reading for December and a November JOLTS - Job Openings Report that showed a noticeable increase in job openings.

The added wrinkle in the ISM Services PMI is that it also featured a notable pickup in the Prices Index (to 64.4% from 58.2%), which topped the 60.0% level for the first time since January 2024.

The data also included a below-consensus ADP Employment Change report for December (122,000; consensus 131,000), and an unexpected drop in weekly Initial Claims (201,000; consensus 218,000; prior 211,000).

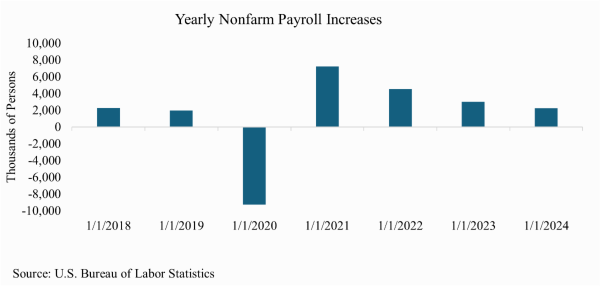

The December employment report featured a 256,000 increase in nonfarm payrolls and a dip in the unemployment rate to 4.1% from 4.2%.

There was also a notable jump in year-ahead and long-run inflation expectations in the preliminary January University of Michigan index of Consumer Sentiment.

These are all positive for the economy but suggest more evidence that the Fed could pause further rate cuts.

Market participants also received the FOMC Minutes for the December 17-18 meeting, which echoed Fed Chair Powell's remarks in his press conference after the meeting. The minutes conveyed a belief that the Fed should hold off on another rate cut until it has more confidence in inflation returning to its 2% target and/or more concern about the labor market deteriorating in a more pronounced manner.

This is nothing new… the Fed makes decisions that are data centric. We get PPI and CPI this week.

Some market experts are even considering the possibility of a Fed tightening in 2025 now, if inflation perks back up?It is way too early to consider that in our view, and global rates should influence our domestic rates… our interest rates are quite high from a global perspective.

Most stocks participated in the broad retreat last week.

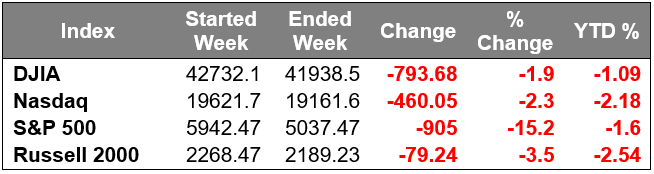

The market-cap weighted S&P 500 dropped 1.9% and the equal-weighted S&P 500 dropped 1.7%.

The Nasdaq Composite fell 2.3% and the Dow Jones Industrial Average closed 1.9% lower than the previous Friday. The S&P 500 briefly traded above its 50-day moving average last week before dropping back below that key level.

Only three S&P 500 sectors closed higher and eight closed lower than last Friday. The health care (+0.5%), energy (+0.9%), and materials (+0.1%) sectors closed higher while the rate-sensitive real estate sector logged the largest decline, dropping 4.1% from last week.

This week will unofficially begin the fourth quarter’s earnings season.

A handful of companies including Delta Air Lines, Walgreens, and Constellation Brands reported last Friday. Several large banks and other financial companies will continue to get the ball rolling this week.

We will hear from JPMorgan, Wells Fargo, Goldman Sachs, and BlackRock to name a few. According to FactSet estimates, earnings for S&P 500 companies are expected to grow by 11.9% year-over-year.

Have a great week!

Michael D. Hilger, CEP®

Managing Director

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.