The Week In Review: 12/30/24

“When people are intimidated about having their own opinions, oppression is at hand.”

– Jimmy Carter

Good Morning ,

We hope everyone had a safe and Happy Holiday!

The stock market limped through the Holiday shortened week but was able to log some minor gains. Volatility was profound, again. The equity market closed at 1:00 p.m. ET on Tuesday and remained closed on Wednesday for Christmas Day.

The so called "Santa Claus rally" period (i.e. the last five trading days of the year and the first two trading days of the new year) began on Tuesday and doesn't always lead to gains in the stock market, but usually features a positive skew. The S&P 500 did close 0.7% higher on the week, the Dow Jones Industrial Average settled 0.4% higher than the previous Friday, and the Nasdaq Composite was 0.8% higher last week.

Santa has been a bit of a Grinch thus far in the stock market, but we still have some trading left.

There wasn't a lot of market-moving news and volume was thin ahead of another abbreviated week. The equal-weighted S&P 500 also settled fractionally higher than the previous week.

Gains in some mega caps and chipmakers provided some support to the broader equity market. NVIDIA closed 1.7% higher, Tesla gained 2.5%, and Broadcom surged 9.5%.

Qualcomm was another winner from the semiconductor space after jurors found that the chip company didn't violate terms of its agreement covering Arm Holding's designs. Shares settled 2.9% higher than last Friday.

Eli Lilly was another story stock, closing 2.0% higher for the week, after the FDA approved Zepbound (tirzepatide) as the first and only prescription medicine for moderate-to-severe obstructive sleep apnea in adults with obesity.

The economic calendar was light, featuring a better-than-expected weekly jobless claims report. Weekly initial jobless claims for the week ending December 21 checked in at a lower than expected 219,000 (consensus 232,000) while continuing jobless claims for the week ending December 14 hit their highest (1.910 million) since November 13, 2021.

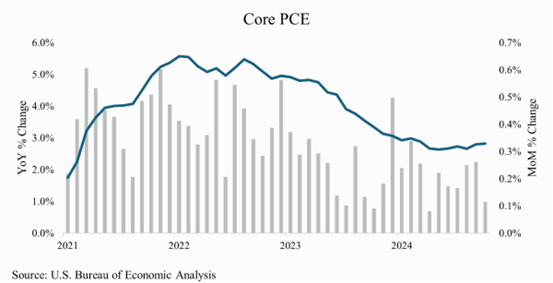

Adding to last week’s anxiety was inflation news…

Inflation stalled on its way to the Fed’s 2% target. Great progress was made in 2023 and the beginning of 2024, but disinflation slowed in the second half of the year.

The labor market showed signs of weakening. Hiring slowed during the year and unemployment surpassed 4%. Wage growth, however, exceeded inflation for the majority of the year creating real wage growth for workers.

The housing re-sale market had the lightest volume since 1995. Housing prices came down slightly after peaking in 2023, but housing affordability remains historically low.

All these factors will play into the Fed’s monetary policy decisions. Now that the Fed is cutting rates, the continued pace and reaction by the overall economy will be a core focus in the new year.

This week will also be shortened with markets closed on Wednesday to celebrate the new year. We anticipate trading volume to again be light again before getting back into the regular groove next week.

We will still receive several economic reports this week. Pending Home Sales will be released on Monday, Manufacturing PMI will be released on Thursday, and ISM Manufacturing will be released on Friday.

Have a safe and Happy New Year!!

Michael D. Hilger, CEP®

Managing Director

Senior Vice President, Wealth Management

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.

If you would like to be removed from this e-Mail Alert Notification, PLEASE click the Reply button, type "remove" or "unsubscribe" in the subject line and include your name in the message, then click Send.