The Week in Review: 12/09/24

“Knowledge speaks, but wisdom listens” – Jimi Hendrix

Good Morning,

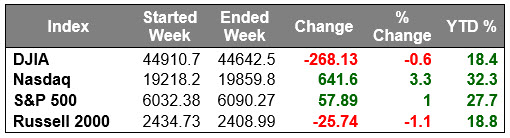

Last week was a big week for the stock market, well at least for the “Mega Caps” … which dominated trading. Their influence was plain to see in the outperformance of the market cap-weighted S&P 500 (+1.0%) versus the equal-weighted S&P 500 (-1.3%).

Our markets were led by the likes of Apple, NVIDIA, Microsoft, Tesla, and Amazon.com.

In addition to some energy from an AI trade that was ignited by Salesforce's encouraging outlook for its Agentforce AI system for enterprises.

Stocks languished on Thursday, albeit after a run that saw the S&P 500 score 11 gains in 12 sessions and set several new record highs in the process.

The latter point notwithstanding, this was not a week accented with broad-based buying interest. The broader market took a backseat to the mega-cap trade and gave in to some consolidation activity.

There were only three S&P 500 sectors that finished higher last week. The upside for the market is that they carried a lot of weight and registered big gains.

The consumer discretionary sector (+5.9%) led the charge followed by communication services (+4.1%), and information technology (+3.4%).

The other eight sectors had a tough go of it… the consumer staples sector, which declined 0.8%, lost the least amount of ground. Otherwise, losses ranged from 1.8% (financials) to 4.6% (energy).

Similarly, while the market cap-weighted S&P 500 gained 1.0% (rounding up), the Russell 2000 declined 1.1% and the S&P Midcap 400 Index fell 1.0%.

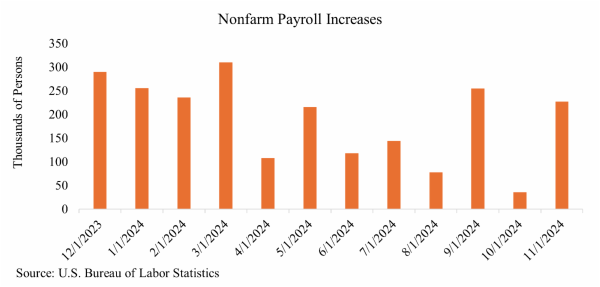

On a brighter note, the S&P 500, and Nasdaq Composite both finished the week at record closing highs, holding their bullish disposition after a November employment report that was neither too hot nor too cold.

The U.S. economy added 227,000 jobs in the month of November, exceeding analyst expectations. September and October’s reports were also revised upwards by 32,000 and 24,000 respectively.

In effect, it was just right for the soft landing/no landing view that left the market hopeful about continued earnings growth and another rate cut at the December 17-18 FOMC meeting.

The CME FedWatch Tool now predicts a probability of 85.8% for a ¼ cut in the Fed Funds rate.

Treasuries also had another winning week. The 2-yr note yield fell six basis points last week to 4.10% while the 10-yr note yield dropped three basis points to 4.15%.

Chairman Powell spoke last week stating that “the economy is not sending any signals that we need to be in a hurry to lower rates.” If the FOMC decides to cut rates again next week, it could be the last one for a while as the economy digests the flurry of cuts and the Fed collects new data.

We will also get a better understanding of the Fed’s position and outlook next week during Chairman Powell’s speech and the release of the Summary of Economic Projections.

Earnings reports this week will be extremely light with only a few stragglers left to announce their results for the third quarter. We will hear from AutoZone, Adobe, Broadcom, and Costco.

For economic reports, this week, we will receive November’s CPI and PPI reports.

These will be the last inflation reports to feed into the Fed’s decision next week. While inflation has taken a step back from center stage, it is still an important data point for the Fed to analyze.

Have a wonderful week!!

Michael D. Hilger, CEP®

The opinions expressed herein are those of Michael Hilger and not necessarily those of Raymond James & Associates, Inc., and are subject to change without notice. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

The information contained herein is general in nature and does not constitute legal or tax advice. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. The Dow Jones Industrial Average (INDU) is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The Dow Jones Transportation Average (DJTA, also called the "Dow Jones Transports") is a U.S. stock market index from the Dow Jones Indices of the transportation sector, and is the most widely recognized gauge of the American transportation sector. Standard & Poor's 500 (SPX) is a basket of 500 stocks that are considered to be widely held. The S&P 500 index is weighted by market value, and its performance is thought to be representative of the stock market as a whole. The S&P 500 is an unmanaged index of widely held stocks that is generally representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs and other fees, which will affect investment performance. Individual investor’s results will vary. The NASDAQ Composite Index (COMP.Q) is an index that indicates price movements of securities in the over-the-counter market. It includes all domestic common stocks in the NASDAQ System (approximately 5,000 stocks) and is weighted according to the market value of each listed issue. The NASDAQ-100 (^NDX) is a modified capitalization-weighted index. It is based on exchange, and it is not an index of U.S.-based companies. The Russell 2000 index is an unmanaged index of small cap securities which generally involve greater risks.

U.S. government bonds and Treasury notes are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return, and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury notes are certificates reflecting intermediate-term (2 - 10 years) obligations of the U.S. government.

The companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapit obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Dividends are not guaranteed and must be authorized by the company's board of directors.

Diversification does not ensure a profit or guarantee against a loss.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.

The companies engaged in the communications and technology industries are subject to fierce competition and their products and services may be subject to rapid obsolescence.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Charts are reprinted with permission, further reproduction is strictly prohibited.