August Client Newsletter

Tech loses its balance

The month of July and August of have been somewhat of a whirlwind from Politics to the market.

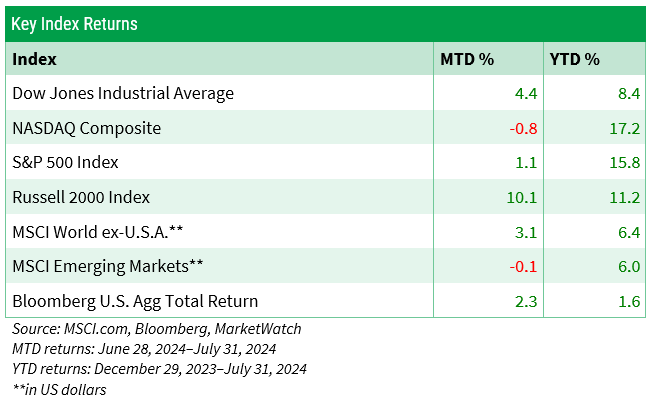

On July 10, the Nasdaq Composite hit a fresh, all-time high—one of many highs recorded this year. But after the 10th, the ride turned bumpy, and the tech-heavy index lost 8% over the next three weeks (Yahoo Finance, through July 30).

What weighed on tech?

A cooler-than-expected inflation reading in mid-July boosted rate-cut speculation.

However, the encouraging inflation figures and discussions about interest rate cuts did not lead to further advances in tech stocks. On the contrary, the opposite occurred.

Tech stocks experienced a sell-off as investors shifted away from this year's top performers, while the Russell 2000 Index, which represents smaller companies that had been struggling, experienced a sudden surge of 10.1% in July.

Smaller companies are more vulnerable to higher interest rates than larger firms and stand to disproportionately benefit if rates fall. Why?

Smaller firms have greater exposure to shorter-term floating-rate debt. Thirty percent of the debt of the Russell 2000 is floating rate, compared with 6% for the S&P 500, according to Goldman Sachs research from earlier this year (Wall Street Journal).

A July 31 story by MarketWatch pointed out that “the small-cap Russell 2000 has outperformed the Nasdaq Composite in July by 11.19 percentage points, on pace for its largest monthly outperformance since February 2001.

“Against the S&P 500, the small-cap index is poised for its best outperformance since February 2000.”

On the last day of the month, Fed Chief Jerome Powell explicitly said that a September rate cut is on the table.

Investors may also be questioning the significant amount of cash that’s being invested in AI and its eventual impact on profitability. However, unlike many firms that failed to survive the dot-com bubble, today’s tech giants are profitable.

Be that as it may, valuations may have gotten a bit extended, and the seemingly continuous rise in tech led to a detour of sorts in July.

Still, the Russell 2000 Index remains 7.7% below its all-time November 2021 high (Yahoo Finance), while the Dow, the S&P 500, and the Nasdaq have repeatedly set new highs this year.

As we enter August, investors are scrambling to see whether this is a short-term blip or if a sustainable rotation into the market laggards is underway.

Economic worries that entered the picture as August began injected volatility into all sectors, especially smaller-company stocks.

Calendar quirk

August and September have historically been unkind to investors, as they sport the two worst average monthly returns for the S&P 500 Index.

Since 1970, the average monthly return for the S&P 500 Index (excluding dividends) has been 0.09% during August and -0.96% in September, according to S&P 500 data provided by the St. Louis Federal Reserve.

Many have offered various reasons why August and September have historically underperformed, but few answers are truly satisfying.

Yet, we’d caution against attempting to time any historical seasonal trends that may or may not surface this year. Weakness in August is far from guaranteed. Since 2010, the S&P 500 in August rose in 2012, 2014, 2017, 2018, 2020, and 2021.

Instead, we recommend a well-diversified portfolio that helps mitigate market downturns but also keeps you positioned to participate in market upswings.

Your strategy should align with your financial goals, investment timeline, and risk tolerance. While we won’t discount the possibility of volatility over the next two months (for that matter, we’d never dismiss the possibility of a pullback in any season), we encourage you to keep your focus on your long-term financial goals.

I trust you have found this review to be informative. If you have any inquiries or wish to discuss other matters, please don’t hesitate to contact me or any team member.

With August starts College season!

A four-year college degree is expensive. How expensive? While the numbers vary depending on whether you attend a public or private university, or in-state or out-of-state institution, the data are sobering.

The average cost of college is $38,270 per student per year, according to Education Data Initiative, a team of researchers that collects data and statistics about the U.S. education system.

The average in-state student attending a public four-year institution and living on campus spends $27,146 for one academic year, or $108,584 over four years. The average cost of in-state tuition is $9,750 per year; out-of-state tuition averages $27,457.

Out-of-state students pay an average of $45,708 per year or $182,832 over four years.

The average private, nonprofit university student spends $58,628 per academic year living on campus, including $38,768 for tuition and fees.

It is not surprising that the average cost of college has more than doubled since 2000.

That may be one reason why college enrollment peaked at 21 million in 2010 and gradually declined to 18.9 million in 2023, according to Statista. The good news is that enrollment is expected to gradually increase as the decade progresses.

It’s easy to point fingers and play the blame game for the meteoric rise in the price of higher education. While today’s costs are daunting, there are steps you can take that will ease the financial burden.

1. Federal aid—What is the FAFSA, or Free Application for Federal Student Aid? The FAFSA is a free form you can submit online or by mail to apply for financial aid. The 2025-26 FAFSA is expected to be available on October 1, 2024. The 2024–25 FAFSA form launched on December 31, 2023, not October 1.

Why FAFSA? Every year, the Department of Education awards billions of dollars in financial aid to college and graduate students via grants, loans, work-study programs, and scholarships.

If you require financial assistance to further your studies, you must submit the form. If you wish to continue receiving aid, you must also resubmit the form every year.

It is best to file as soon as you can. Financial aid is distributed on a first-come basis, first-served basis. When the money runs out, well, it runs out. Wait, and you may miss out on valuable grants and resources.

In addition, aid from schools may have earlier deadlines than federal financial aid, so don’t delay.

2. Leverage your skills through scholarships. There are athletic, academic, extracurricular, and student-specific scholarships. Some of these include identity-based scholarships, legacy scholarships, religious scholarships, and first-generation scholarships. Are you the first in your family to attend college? You may qualify for assistance.

Other scholarships include need-based scholarships, employer scholarships, STEM scholarships, and military scholarships.

If you are currently in high school, talk with your guidance counselor. Better yet, get to know your counselor. He or she may be able to recommend aid that's a good fit for you.

And don’t stop there. You are in a scavenger hunt for funding; you are geocaching for college cash.

Are you a member of a national club or a church? Are your parents members of a union or civic organization? Many of these groups offer scholarships to members and their children.

The Rotary Club, Kiwanis Club, Chamber of Commerce, local churches, and foundations may offer scholarships based on a variety of factors and needs. People enjoy helping others, especially when a young man or lady approaches them and is resourceful, mature, and has a positive outlook on life.

Local scholarships are usually funded by community organizations and businesses that want to see their local students thrive. Besides, there’s often less competition for these scholarships.

But success in college is more than simply grappling with finances.

3. What school would you like to attend? Choose carefully. Some students know exactly what they want, and they apply to colleges that meet their criteria. Others have yet to decide on a career path or what they really want from a college.

Nonetheless, you probably have a general idea of the school you might want to attend. Do you prefer a large school, or does a smaller campus better suit your personality? Do you gravitate to an urban setting in a big city environment? Or do you prefer recreational opportunities, the outdoors, and a more rural setting?

Get out and visit the schools that interest you. Talk with current students, see the campus and facilities, chat with professors in the major you are considering, and visit the dorms. You’ll quickly find out whether the school is a fit.

Who are you?

4. Your essay, your story. Most selective college applications will require an essay—a narrative within the context of the question asked on the application.

You are unique, and the best way to tell your story is to write a thoughtful essay about something impactful or meaningful to you.

Admissions officers read countless essays. They know this can be a difficult project, and it’s easy to get lost in the shuffle. Be you, be genuine, and don’t be afraid to be vulnerable. Don’t try to write about something you really aren’t interested in but believe will impress the admissions officer.

Admissions officers are simply looking for motivated students who will add that special something to their freshman class, according to The Princeton Review.

Start early and write several drafts. Have someone edit your application. Another set of eyes is always a plus.

And don’t simply retell the story. Anyone can give a play-by-play of an event—we went overseas, we helped build a home, we played games with the local kids, etc. Take some time to reflect on your experiences. Share what you gained, how it impacted you, and how it shaped you.

Preparing for college involves more than just academic strength; it’s about developing the skills and mindset that will help you thrive in your new environment. Embrace the opportunities and challenges that will surely come your way. Creating a plan and taking steps to move forward will allow you to write the next chapter of your life with confidence.

If you have questions about your funding goals, please let us know. We want to help you succeed!

As always, thank you for choosing us as your financial advisor. We are honored and humbled by your trust.

Sincerely,

Cheryl L, Myler, CRPC

Vice President-Wealth Management

Content prepared by Horsesmouth for use by Financial Advisors'.

Any opinions are those of the author and not necessarily those of Raymond James. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional.

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal. The NASDAQ composite is an unmanaged index of securities traded on the NASDAQ system. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index. The MSCI ACWI ex USA Investable Market Index (IMI) captures large, mid and small cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 24 Emerging Markets (EM) countries*. With 6,211 constituents, the index covers approximately 99% of the global equity opportunity set outside the US. The MSCI Emerging Markets is designed to measure equity market performance in 25 emerging market indices. The index's three largest industries are materials, energy, and banks. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market.