Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- The U.S. Economy continues to be a global growth leader

- Tariffs pose a bigger risk to the European growth outlook

- U.S. equities have maintained superior fundamentals

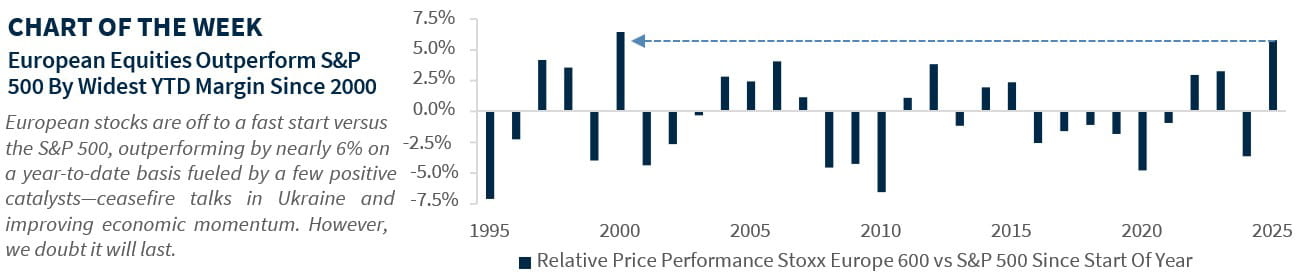

February 24 marks the third anniversary of the Ukraine/Russia war. While initial expectations were for a swift resolution, the war has become a prolonged and costly struggle, impacting millions of Ukrainians and causing widespread global repercussions. President Trump's recent efforts to mediate an end to the conflict have led to a resurgence in European stocks, which are experiencing their best start to the year versus the S&P 500 since 2000. This comes after a period of underperformance, during which Europe lagged the US in ten out of the last twelve years. Additionally, the debut of China's AI model on the global stage has prompted some investors to reassess the concept of 'American Exceptionalism.' This raises the question: are European equities poised for a sustained recovery relative to U.S. equities? Below, we outline five reasons why, as long-term investors, we continue to favor U.S. equities over European equities:

Five Reasons Why We Still Favor The U.S. | Despite Europe’s recent outperformance, below are five reasons why we still favor US equities:

- U.S. Economic Growth Remains On Top—The U.S. economy continues to be a global growth leader, significantly outperforming its European counterparts. The US is projected to grow 2.4% in 2025, compared to the 1.0% growth rate expected in Europe. While recent developments, such as France passing its 2025 budget, upcoming elections in Germany potentially leading to more expansionary fiscal policies, and ongoing peace negotiations in Ukraine, have boosted European stocks, these short-term catalysts may not sustain the recent momentum. From our perspective, Europe's structural challenges—such as low productivity, excessive regulation, and intense competition from China—suggest that its growth rate will likely continue to lag that of the US. Consequently, this lower growth is expected to result in weaker earnings growth for European companies.

- Tariffs Pose A Bigger Risk To Europe—President Trump's tariff threats have heightened global economic uncertainty, as reflected by record highs in both the global economic policy uncertainty and trade uncertainty indices. If trade tensions escalate further, Europe would likely be more affected than the US. Economically, the US is more self-sufficient and service-oriented, relying less on trade goods, whereas Europe is more dependent on trade. Exports account for ~50% of Europe's GDP, compared to just 11% in the US. From a revenue perspective, companies in the Stoxx Europe 600 generate only 33% of their revenues domestically, while S&P 500 companies derive ~60% of their revenues in the US. This domestic focus suggests that the US would be less impacted than Europe if trade tensions intensify.

- US Boasts Superior Fundamentals—One of the strongest arguments for investing in Europe is its attractive valuations. As of early 2025, the Europe Stoxx 600 Index was trading at its largest discount relative to the US in at least 30 years. However, the US boasts superior fundamentals that justify a widening premium for its stocks. For instance, the US is projected to achieve higher EPS growth in 2025 compared to Europe (13% vs. 10%) for the third consecutive year. Additionally, US companies have higher net margins (13.1% vs. 10.1%) and are expected to see stronger dividend growth for the third straight year. Moreover, the US has a robust infrastructure that fosters innovation. Approximately 50% of global venture capital investment occurs in the US, compared to just 20% for all of Europe. This has led to the creation of ~90 publicly traded companies with market caps exceeding $50 billion in the US over the past 50 years, compared to just 13 in Europe. Overall, these factors should continue supporting US outperformance and maintaining its premium valuation over Europe.

- Sector Preferences Still Favor U.S.—Sector composition has been a tailwind for Europe YTD; however, this trend is not expected to last. European stocks have benefited from the strong performance of Financials, the largest sector within the Stoxx Europe 600 Index, which has a 22% weighting. In contrast, Tech, the largest sector in the S&P 500, has been the second worst-performing sector YTD. While these sector differences have supported European stocks in the near term, this is likely to be short-lived. The long-term outlook for Tech remains positive due to superior earnings growth, continued investment in AI, and healthier margins. With Tech comprising ~32% of the S&P 500 compared to just 8% in Europe, the expected tech resurgence favors the US. Additionally, our three favored sectors—Tech, Industrials, and Health Care—make up ~50% of the US market versus ~40% in Europe, further supporting a preference for US equities over European ones.

- Technicals Suggest A Pullback Is Likely—European equities have surged since the start of the year, with the Stoxx Europe 600 Index up ~10% in USD terms, outperforming the S&P 500 by ~6%. Following last year's historic underperformance, where European stocks lagged the S&P 500 by their widest margin on record (~22% in 2024), investors have shifted into European stocks to capitalize on historically attractive valuations. This rotation has been supported by recent fund flows. With peak pessimism on Europe likely priced in, a few positive catalysts—such as potential ceasefire talks in Ukraine and the euro zone’s Citi Economic Surprise Index reaching a 10-month high—have triggered a significant positive market reaction. However, the strong gains in European stocks YTD have pushed momentum indicators into overbought territory (14-Day RSI > 70), suggesting that further gains may be challenging without additional clear positive catalysts.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.