Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Many investors are wondering what to think of the volatility and uncertainty that has been pulsing through financial markets over the past few weeks. My crystal ball is no clearer than anyone else’s, so I will not be offering any predictions about how the tariff situation is going to play out. What I do know is that yields were at attractive levels a month ago and intermediate and long-term yields have pushed higher from there. For investors, this means that there are opportunities across the fixed income landscape to purchase bonds at attractive yields. Yield curves have steepened recently, adding additional value out further on the curve.

The move higher in municipal yields has pushed most of the curve to levels that have only been available for a few brief time periods over the past 10+ years. The overall attractive yields combined with the positive slope of the curve means that intermediate and long-maturity municipal bonds offer considerable value, especially for investors in high tax brackets. 4% coupon bonds at or below par can be easily found, while some 5% coupons at or near par have been available recently. Opportunities to purchase high-quality municipal bonds at these yield levels do not present themselves often and tend to disappear quickly.

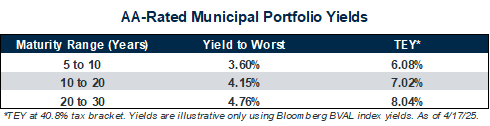

To highlight the opportunity that is currently available in municipal bond portfolios, the table below shows a few sample AA-rated portfolios and the corresponding yields that they offer. Good value is available across the curve, but note the increase in taxable equivalent yield (TEY) of ~200 basis points when moving from the 5 to 10 year portfolio to the 20 to 30 year portfolio. A TEY of over 8% for a AA-rated portfolio is compelling for investors looking for attractive returns combined with high credit quality. Over the past 50+ years, AA-rated municipal bonds have a “non-default rate” of 99.98% over an average 10-year timeframe (Source: Moody’s Default Study, 1970-2023).

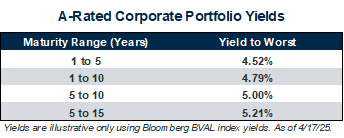

For lower tax bracket investors or qualified accounts, corporate bonds offer similarly attractive value. The table below highlights yields available for A-rated portfolios across a range of maturity spectrums. Intermediate-term bond ladders offering 5% yields or better typically meet or exceed most investor targets for a high-quality fixed income portfolio. For those investors following the 4% withdrawal rate rule-of-thumb, these portfolios can exceed that target by 100 basis points or more. Also, keep in mind that these illustrations show A-rated portfolios. Moving down slightly on the credit spectrum into still-investment-grade, high-quality BBB-rated bonds provides additional yield to investors.

Timing the market and finding the perfect entry point is a good idea if your crystal ball is working perfectly. For the rest of us who do not know exactly how the next 6 to 12 months are going to play out for the global economy, locking in the attractive yields that are currently available could set up your portfolio for long-term success. This opportunity might last 5 more years or 5 more days. If you can lock in yields today that will help you achieve your long-term financial goals, why wait?

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.